Supreme Thwart

Railroad Weekly February 23, 2026

Inside This Issue

· Supreme Thwart: Top U.S. Court Rules Tariffs Illegal

· But No Day to Par-Tay: Tariff Man Sees Another Way

· Second Time Around: UP to Refile Merger App Apr. 30th

· Your Price is My Slice: CN, CP Eye Access to UP Network

· Low Growth, No Problem: RRs Don’t Need a Boom to Bloom

· Give Me Just a Little More Climb: CSX Glad w/ Just Modest Growth

· Off to See the Blizzard: RR Crews Prep for Eastern Storm

· This Week: Numbers for Berkshire and BNSF

Track Talk

“We’re in the fourth year of a freight recession. I don’t think there’s ever been a four-year freight recession before.”

-Canadian National Tracy Robinson

The Latest

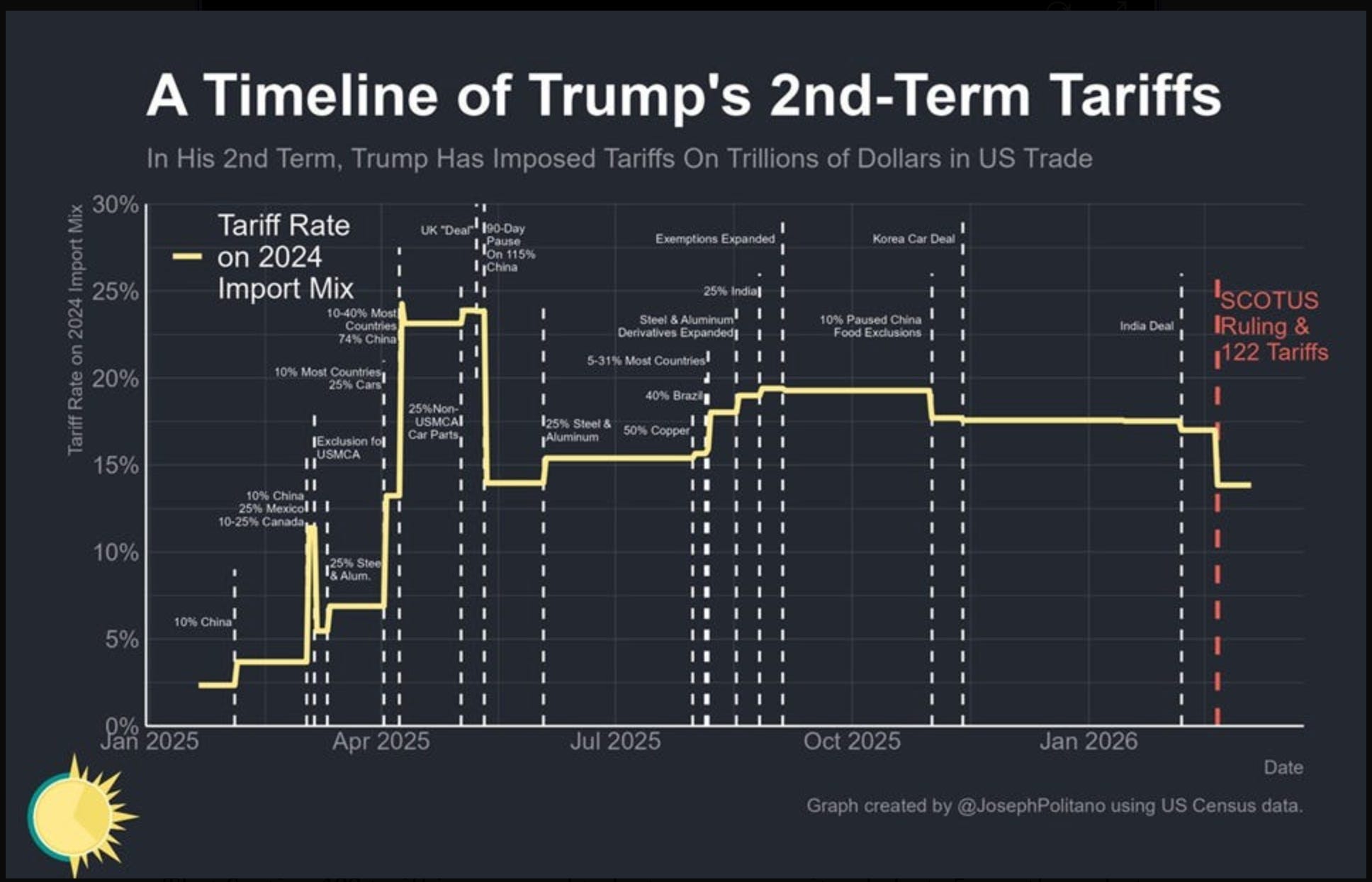

· “We hold that IEEPA does not authorize the President to impose tariffs.” With those words, the U.S. Supreme Court ruled President Trump’s emergency tariffs illegal and void. IEEPA refers to the 1977 International Emergency Economic Powers Act, which the White House invoked as justification for broad tariffs, initially on Canada, Mexico, and China, and later (“Liberation Day”) on all countries. The emergencies cited were illegal drug flows and “large and persistent trade deficits.” Importantly however, the ruling does NOT apply to other tariffs currently in place, most importantly the “Section 232” tariffs on autos, lumber, and metals (steel, aluminum, and copper). Those have been at least as problematic for railroads as the IEEPA tariffs. The IEEPA tariffs had their biggest impact on intermodal demand.

· The story is far from over. President Trump reacted to the Supreme Court ruling by immediately announcing a blanket 10% tariff—which a day later became 15%—on all countries starting this week. He’ll base those on a different law than IEEPA: the Trade Act of 1972. But there are lots of caveats. Canada and Mexico it seems, will still enjoy a temporary exemption for imports covered by the USMCA trade pact (which is currently up for renegotiation). The USMCA exemption applies to most cross-border trade flows but does not shield businesses from the Section 232 tariffs.

click here for a clearer version of the graphic below:

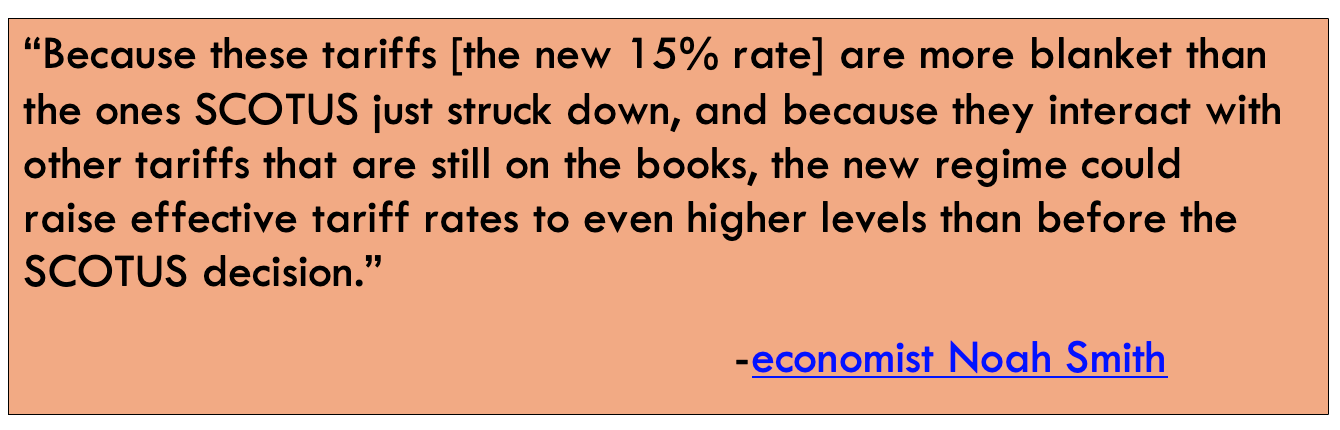

· While a relief to companies in one sense, the Supreme Court’s ruling introduces new questions without clear answers. How will tariff refunds be administered? Will this be a complicated and expensive process requiring lawyers and consultants? If so, will smaller businesses even bother? What about the many small businesses already bankrupted by the tariffs? Will there be any recourse for them? In the meantime, President Trump says he plans additional tariffs soon. As you can see, the bureaucratic spider web of tariffs—and all the cost and uncertainty surrounding it—remains as bureaucratic, costly, and uncertain as ever.

Other Developments

· As tariff chaos ensues, Union Pacific and Norfolk Southern continue to rework their merger application to comply with STB demands. Last week, they said to expect a re-submission on April 30th. That’s a little over a month from now, giving more time for rival railroads to hone their strategic response. One thing rivals are focused on: What concessions should they ask for, i.e., that UP and NS should grant trackage rights in a specific geography. Some are surely licking their lips as they contemplate more access to UP’s prized Gulf Coast chemical business.

· Look at those railroad stocks—up again last week, boosted this time by the Supreme Court ruling. The sector is also benefitting from the broader trend of investors shifting their capital away from software firms potentially threatened by AI. Speaking of AI, remember that IT products—including those critical Nvidia chips imported from Taiwan—have been largely exempt from tariffs.

· This could be a challenging week weather-wise for eastern U.S. railroads. As of Sunday, winter storm Hernando was threatening heavy snowfall, strong winds, and sub-freezing temperatures throughout the northeast and mid-Atlantic regions. Norfolk Southern, for one, said it was “monitoring and preparing for Winter Storm Hernando… proactively preparing equipment, scheduling crews, and evaluating customer and terminal readiness to combat the impacts of this event.”

· An update from the railcar market: GATX, a top lessor, reported earnings last week, highlighting the unusually low level of new railcar production right now. At the same time, more railcars are exiting fleets, due in part to “supportive” scrap rates. “As a result, we’re seeing net fleet shrinkage in the North American fleet… That’s a positive when you’re the largest owner of railcars in North America.” GATX just got a lot bigger, remember, with the acquisition of Wells Fargo’s railcar portfolio. Management did clarify that it’s not seeing railcar shortages. It did say some fleet types, notably box cars, become less valuable when the industrial economy is soft, as it has been during the past few years. GATX, however, has more of its exposure with cars handling heavy haul bulk traffic, like tank cars and specialty covered hoppers. They’ve performed well in terms of lease rates and utilization.

· Here’s an interesting niche railroad story from Alaska, courtesy of KTUU in Juneau. The Alaska Railroad, with about $200m in annual revenue and roughly 1k freight cars, said it’s committed to facilitating construction of a big pipeline project. But before it invests in additional railcars and other upgrades, the railroad wants more assurances that the pipeline will actually be built. Oil and gas are critical to Alaska’s economy, as are tourism, seafood, and the U.S. military.

· This Saturday (Feb 28th), Berkshire Hathaway will report it Q4 and full-year financial results. They’ll include, of course, figures for BNSF. Berkshire does not hold earnings calls. It will, however, publish CEO Greg Abel’s first annual letter to shareholders. It’s a tradition famously practiced for decades by the legendary Warren Buffett, who’s still the company’s chairman.

Conference Highlights

Union Pacific

· The campaign continues. The Union Pacific executive team was on the road again last week, pitching the merits of its merger. At a Barclays investor event in Miami, CEO Jim Vena again made his case that combining UP with Norfolk Southern will be good for shippers, good for workers, good for the environment, good for the economy, and so on. He again discussed the opportunity to grow, competing for new business in watershed markets, for example. He addressed concerns about operational risks, highlighting UP’s success implementing its NetControl system. Class I railroad partnerships, he reiterated, are welcome but, “The history will tell you… those things don’t last.” Inevitably, they’re hung up on disagreements over how to allocate resources like locomotive time and fuel.

· Vena is a man in a hurry. He’s still confident of closing the deal in the first half of 2027, despite the STB’s initial rejection of UP’s application. The clock won’t restart until resubmission, likely on April 30th. The STB will then have up to 90 days to accept comments from others. “Hopefully, the STB looks at that and says they don’t need the 90 days for that and gives them 45 days, because they’ve already been looking at that application for a while.” In-person hearings would likely follow. Then, “there could be back and forth before we get to the end.” Ultimately, Vena is confident that the STB will see the logic of the merger, and the ample benefits it would bring. “It’s a great deal for America.”

· He wishes, to be sure, that the process was faster. “Listen, it’s different than the way I do business. I made a decision on some stuff that we’re buying for our company. And I think it took me 20 minutes last night… We understand. But we also want to try to speed it up. It is what it is.”

· Not for the first time, Vena attributed the criticism of rival railroads to their own fears—fears about how strong a competitor a combined UP and NS would be. They now feel “they have to do something.” And so, they’ll push the STB for concessions. “But that’s not the STB’s job, to close that gap for them financially. It’s their job to make sure that the competition is out there.” And this is not 1890, when railroads moved the majority of America’s freight. Today, “railroads make up about 13% of the total movement of goods in the U.S.”

· Canadian National, he asserted, worries what the merger might do to its auto business, for example. “We’re going to be more competitive into Michigan and Ohio and the southeast, right?” CSX, he continued, worries about the implications for its boxcar merchandise business.

· Addressing opposition from CN and CPKC specifically, Vena asked why transcontinental railroads should be allowed in Canada and not the U.S. “Last time I looked, I haven’t seen anybody [say] that they need to split the railroads in two because… they shouldn’t operate across the country.” Separately, he brought up the dispute UP has with CPKC on the Meridian Speedway. “With Canadian Pacific, before they purchased Kansas City Southern, we delivered an 11k-plus foot train to go across the Norfolk Southern over the Meridian Speedway… Now we have to split the train in two pieces and give them max 8,500 feet.”

· When done discussing the merger, Vena and his colleagues discussed the latest demand trends. January’s rough weather caused some disruption, but it was brief. “We’re back at, call it, 230, 240 car miles per day. Our dwell times are sub-20 again.” Carload volumes are currently down about 2% y/y so far in Q1. February is up, however, thanks to strength in bulk markets like grain and coal. Petrochemical markets are also faring well, not because the market is “on fire” but because of new business wins. Domestic intermodal “is still good for us.” Here too, UP is winning new business—and from trucks, not other railroads. Another market doing well right now is construction aggregates.

· Weaker markets include international intermodal, where y/y comparisons are challenging (recall the rush to pull imports forward this time last year). The auto market is weaker but “starting to look a little bit better.” Forestry remains weak too as the housing slump lingers.

· UP isn’t ready to declare a recovery in the industrial economy yet, despite how “people are excited about ISM,” [referring to the bullish ISM manufacturing report for January]. Nor is it ready to declare a revival in intermodal pricing, despite how people are “excited about some of the [recent increase in] truck pricing.” If these trends continue for sure, “we’re in a great position to capitalize on it.”

CSX

· It’s been about five months now since CSX hired Steve Angel to succeed Joe Hinrichs as CEO. Angel’s been mostly quiet early on his tenure, as he learns the railroad business and reformulates the company’s strategy. He did speak at last week’s Barclays event, clarifying his thoughts on various subjects. He’s staying neutral for now on the UP-NS deal, emphasizing that mergers take a long time to play out—joining his old company Linde with Praxair took about three years from announcement to closure. The UP-NS deal, he says, will bring both opportunities and risks to CSX, which has a small team of people at Jacksonville headquarters analyzing the implications. Angel is confident that the STB will listen closely to railroad customers—those for and against the merger.

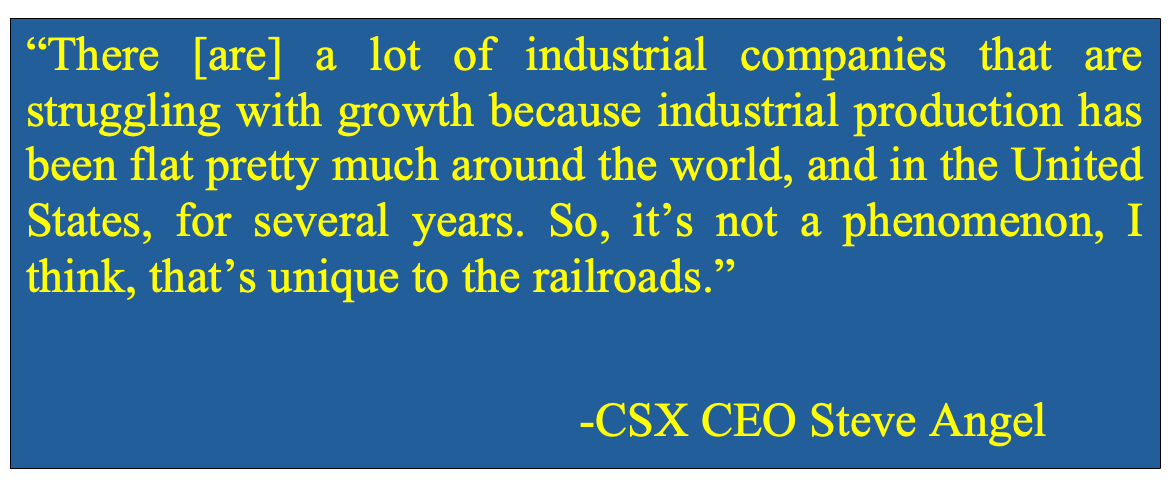

· His focus though, is on running a better, safer, and more profitable CSX. He wouldn’t trade its geographic footprint with any other railroad, mindful that if the U.S. re-industrializes, much of that re-industrialization will happen in regions it serves, like the southeast. Nationwide, the U.S. isn’t seeing much industrial investment yet, which he attributes in part to “tariff noise.” But recent corporate tax cuts, plus the dearth of opportunities elsewhere in the world, positions the U.S. well for future investment. China, he points out, is no longer the investment opportunity for international companies it once was. Europe hasn’t been growing for years. India is growing but nowhere near on the scale of China’s earlier growth. “All roads lead back to the United States.”

· Making himself clear, Angel isn’t waiting for an industrial boom. He understands that many of the sectors CSX serves are mature. “I don’t think of it in terms of, gosh, I need mid-single-digit growth to really be able to deliver the kind of operating performance I want to deliver… A little bit of growth is all we really need.” As it waits for even a modest upturn, CSX can deliver financial improvement by prudently managing costs. “I love growth,” he asserts. “But I trust costs.”

· CSX is telling Wall Street to expect low single-digit volume growth in 2026. And it said, “We’re going to increase operating margins 200 to 300 basis points.” [Note: 100 basis points equals one percentage point; Another note: Like many newcomers to the industry, Angel finds the use of operating ratios—operating margins turned upside down—rather odd.].

· Of course, “if the macro economy blesses us, if housing starts pick back up, automotive picks back up, GDP picks back up... If that happens, then by working so hard on productivity and leaning out our cost structure, I know those margins fall through very heavily.” Put another way, CSX is positioned to earn very strong profit margins on any incremental new business is captures. Remember, a big portion of a railroad’s cost base is fixed, meaning it won’t change even as new revenue is captured. Example: Crew costs won’t change just because you add some more railcars to an existing train. “We just need a little bit of volume growth every year, a little bit of price every year, productivity every year, and we can deliver the kind of result we want.”

· Given his past, nobody knows more about the chemical industry than Angel. That’s divided into many different sub-categories, he explains, but in general, “I don’t think there’s any secret that chemicals has struggled globally. There’s an oversupply situation coming from China that weighs on that industry.” In addition, a lot of chemical demand comes from the housing and auto sectors, both of which are currently weak.

· Coal, at least domestically, “is seeing a little bit of a rebirth.” But he’s quick to caution that it’s still “kind of a mature industry.” Same for forest products. In fact, several CSX-served pulp and paper plants closed last year.

· On the other hand, CSX’s mineral business, “basically rock aggregates that are used to build out infrastructure,” is trending positively. “That’s a market that’s growing for us.” Another bright spot is fertilizers. “We’ve got some new phosphate production that’s come online. That’s helping us.” Intermodal is growing too. In summary, Angel calls the demand situation “a mixed bag.” But again, “I’m not sitting here saying, gee, if you just give me 5% volume, I’ll be fine. I’m sitting here thinking I don’t really need that much.”

Canadian National

· CN’s chief Tracy Robinson addressed the Barclays event as well, while CFO Ghislain Houle spoke at another gathering hosted by Citigroup. Like other Class Is, CN is struggling to grow in a weak economy but delivering strong profits nonetheless thanks to productivity gains and other self-help measures. CN’s exposure to macroeconomic headwinds might be worse than even what other Class Is are experiencing, given the outsized impact of tariffs on some of its most important businesses, like forestry.

· In 2025, CN spent roughly US$250m on tariffs. The U.S. currently has a 45% import tax on Canadian lumber, which is unaffected by last week’s Supreme Court ruling. What’s more, North American housing construction remains depressed, with CN now capturing about 1,300-to-1,350 railcar orders of lumber per week; “In the good years… [we] would be anywhere between 2,300 to 2,500 car orders per week,” Robinson explained. “Lumber is hurting, and lumber is one of the segments that is one of the most profitable for CN.” Nor is she expecting a revival anytime soon.

· It’s hardly all doom and gloom on the demand side though. CN is busy moving last fall’s bountiful grain crop, and grain alone accounts for nearly a fifth of the railroad’s total revenue. “The beauty with grain is it’s not dependent on the economy. People need to eat.” Another important point about grain volumes: While any given year can have a good or bad harvest, thanks to technology and improvements in fertilizers, farmers on average over the past decade have grown their yields by about 2% to 3% annually. Grain, furthermore, “is the only commodity that we’re paid by the ton.” And CN can move a lot of tons on a single train thanks to the latest-generation of hopper cars. “These grain cars are more bulky, so you can put 10% more grain in a car. And because they’re shorter, you can put 8% more car on a train.” Remember too that CN now owns the Iowa Northern shortline, which further ups its exposure to grain revenue.

· Canada’s many other natural resources underpin CN’s future growth potential. Robinson mentioned products from and for the energy and chemical sectors like natural gas liquids (NGLs), plastics, potash, frac sand, and metallurgical coal. Many such opportunities are divorced from the performance of the economy. “We sit on top of most of the significant natural resource base, either in Canada [or] in the midwest through the United States.”

· Less happily, “We’re not expecting the international intermodal volume to be strong across anywhere in North America through the first half of the year.” However, “domestic intermodal continues to grow,” thanks to “really good service.” It also claims to be winning share from trucks. Major investment to expand the port of Prince Rupert will bring new business. Already, the Gemini maritime alliance is offering new Rupert service. Houle gave some more detail, noting that TEU volumes handled at Rupert hit a peak of about 1.3m. Last year was more like 900m. Capacity is about 1.6m. “It’s coming back, but it’s not where it needs to be.” Of course, with the intermodal business more generally, “the big question is where the tariffs go [and] how healthy is the underlying consumer.”

· A key goal is finding new trade flows to replace tariff-hit southbound markets to the U.S. On example is helping CN’s oil customers find new export markets. “CN has an unparalleled port access, going off all three coasts. So, if their markets shift and there’s less oil going south, can we help them explore off the east and the west.” Prince Rupert by the way, is becoming a more important gateway for carload traffic; it’s not just focused on intermodal containers.

· CN managed a 62% operating ratio last year. Can it get back into the 50s, as it last did in 2022? “Under a supportive economy,” Houle declared, “absolutely. I’m very bullish.” Underpinning that confidence is a “much leaner, more nimble cost structure,” plus ample capacity to handle more volume without any major new capital investment. CN also has “locomotives tucked away” and “800 or 900 people furloughed that we’re staying very close to.” It will be ready to pounce, in other words, when the economy turns, or if the tariff situation unexpectedly improves.

· And the UP-NS merger? CN makes no bones about its opposition. “We’re very positive on competition. And we’re very much aligned with the industry on wanting a lighter touch on regulation to make us more nimble and able to invest properly. And this merger application works against both of those things.” UP and NS would together control about half of all U.S. rail freight, Robinson explains. It will reduce competition in some geographies, which contradicts the rule about mergers having to “increase competition.”

Keep reading with a 7-day free trial

Subscribe to Railroad Weekly to keep reading this post and get 7 days of free access to the full post archives.