Mex Marks the Spot

Railroad Weekly August 7, 2023

Photography by Frederick Manfred Simon © www.steelwheels.photography

Inside This Issue

· Mex Marks the Spot: Ferromex Bucks Industry Trend, Improves OR

· CSX In Top Spot: Florida Railroad Leads the Sector in Q2 OR

· Santa Flaws: A Severe Double-Digit Volume Drop for BN Santa Fe

· More Jobs Jolly: U.S. Employment Keeps Growing and Growing

· But Another Fuel Prices Crisis? Bulls Beware: Gas Prices Rising Again

· My Cousin Vena: Some Union Leaders Think He’s a Bad Hire

· Update on the Inventory Story: Schneider Encouraged by De-Stocking Trends

· Chem-Back Kid? Some Encouraging Signs for Chemical Traffic as Well

Track Talk

“As COO, Jim Vena enacted policies, practices, and procedures that deliberately destroyed our members’ quality of life for the sake of profit… He orchestrated huge furloughs and cuts to every department in transportation, which resulted in the crew shortages we have yet to recover from. Vena put this railroad on a long-term path of destruction for a short-term return on investment for Wall Street tycoons.”

-Letter from five Smart-TD union leaders, to UP’s Labor Relations chief (courtesy: Bill Stephens, Trains Magazine)

The Latest

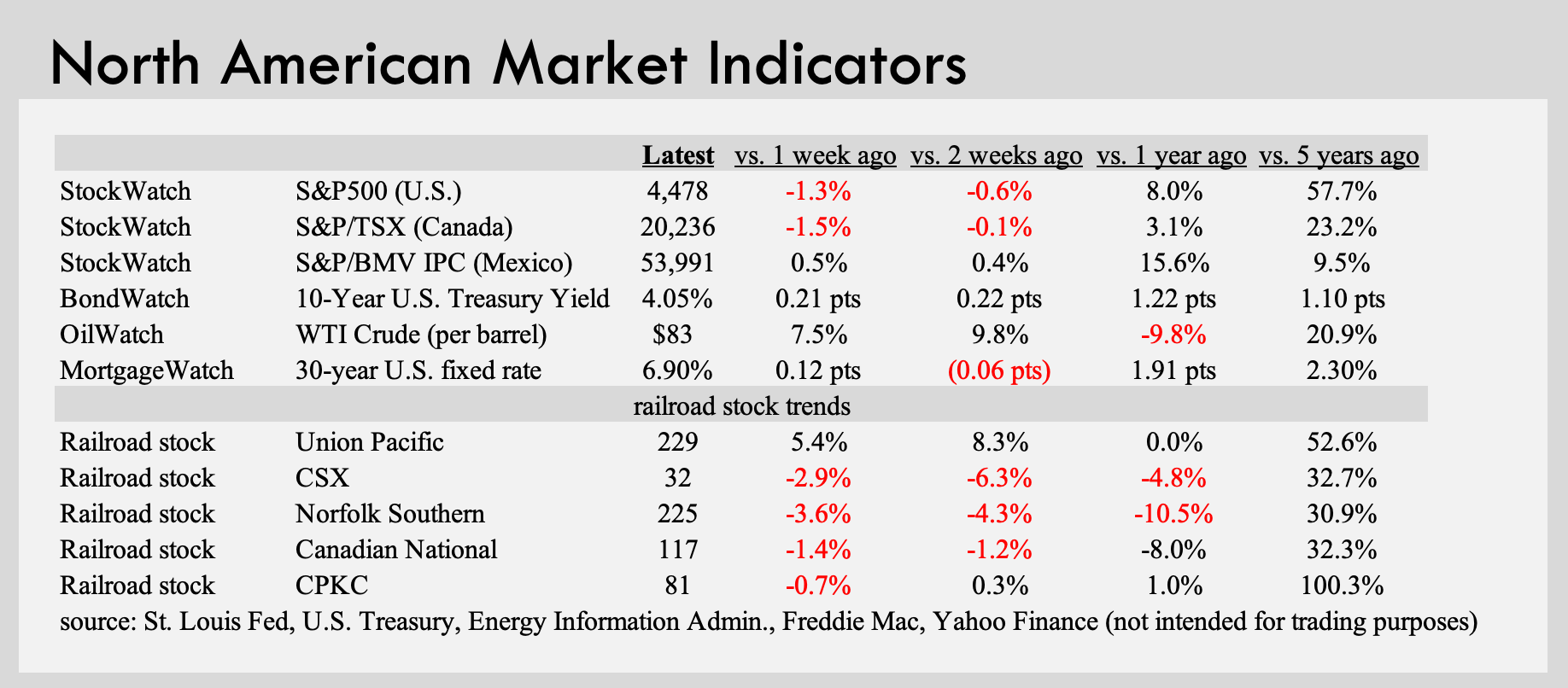

· For North America’s Class I railroads, second quarter earnings season is now complete. The good news: All were profitable. The bad news: Not a single one managed to improve profitability versus last year. CSX did best with a 60% operating ratio. BNSF did worst at 68% (it was worst for all of 2022 as well). Why is 2023 worse than 2022, industry-wide? Railroads are operating more reliably. But there’s less freight to haul. Indeed, all six Class I railroads carried lower volumes during this year’s Q2 than they did in the same quarter last year. Some markets led by autos grew substantially. But not enough to overcome a deep intermodal recession. In Mexico, however, Ferromex bucked the trend and produced both volume and revenue growth. Its profit margins still lag those of its peers to the north. But at least they improved y/y, boosted by the onset of new nearshoring activity in Mexico’s industrial and logistics sector.

· Yet another upbeat U.S. jobs report lent further momentum to the bullish sentiment now prevailing about the U.S. economy. Employers added another 187k jobs in July, nearly half of them in health care and social services (i.e., childcare and eldercare). There were job gains in construction but losses in manufacturing (led by reductions in companies producing chemicals, food, and even autos). Retailers and wholesalers accounted for 14% of July’s job gains. Rail transportation jobs grew by about 2,000, reaching 150,400. But trucking employment shrank, as did warehouse employment. The biggest area of job losses involved temporary workers. Overall, the U.S. economy has added an impressive 3.4m jobs in the past year, 30% of them in health care, education, and social services (where, incidentally, productivity gains are difficult to achieve).

· Some other new data from across the U.S. economy: A report from Challenger, Gray & Christmas said U.S.-based employers announced about 24k job cuts in July, a 42% decrease from June, and an 8% decrease from last July. For the first seven months of 2023, however, they’ve announced 482k cuts, up from just 159k during the same period a year ago. In the same period of 2020, for reference, the figure was 1.8m. Separately, the latest ISM service sector index (based on purchasing manager sentiment) was again in expansion territory. Construction spending grew 3.5% y/y in June (an 18% increase in nonresidential construction offset a 10% decrease in residential construction). Labor productivity was up 1.3% y/y last quarter as output grew faster than the number of hours worked. But this is still below America’s 2.1% average since 1947. Today’s U.S. economy is much more service-oriented than it was in the past, with health care alone accounting for almost a fifth of all output. Productivity gains in health care, as mentioned, are difficult to achieve, not to mention difficult to measure.

· As the healthy job market suggests, the U.S. economy is—so far, anyway—digesting the Federal Reserve’s monetary tightening without too much pain. But warning: rising fuel prices might prove a more potent form of kryptonite. Rapidly declining fuel prices have no doubt boosted consumer spending in the past year. But last week, gas prices rose to their highest levels of 2023, hitting a national average of $3.82 per gallon, according to AAA. That might be a temporary jump, however, the AAA explains, linked to the extreme heat and its impact on refineries. Demand for gasoline, it notes, is trending down. Other economic risks on the radar include a resumption of student debt payments, a potential government shutdown in October, and tightening bank lending standards.

· Back within the rail sector, BNSF is now suing the STB for what it says was a wrongful injunction ordering it to haul more coal for the energy company NTEC. UP stands to benefit as Hub Group announced an expansion in the automotive space, intending to offer intermodal service to all of Mexico’s auto plants. Hub plans to make use of UP’s new Falcon Premium service. It’s been six months now since Norfolk Southern’s East Palestine derailment, with nothing yet as far as rail safety bills passing Congress. FTR’s Todd Tranausky, in his latest weekly rail podcast, notes an encouraging uptick in chemical volumes by rail—“Maybe some green shoots of optimism in the chemical sector.” Canada’s two major railroads, CN and CPKC, outlined their plans to carry this fall’s grain crop, which is looking like it should be another good one. Interestingly, the highly profitable Irish airline Ryanair mentioned in its latest earnings call that its Boeing plane deliveries have been delayed due to the recent collapse of a rail bridge in Montana. The bridge was critical for moving aircraft parts on BNSF between Wichita, a major aerospace hub, and Seattle, site of several Boeing factories. Service has since been restored.

· Speaking of earnings calls, various companies gave commentary on rail service during their Q2 presentations. Warrior Met Coal detailed the recent declines in coal and steel prices, while expressing relief at better rail service. It’s currently developing an Alabama mine that originally planned to rely on river transport to the port of Mobile; it now says it will build a rail link as well. Koppers, a leading provider of rail ties, essentially threatened to leave the business unless railroads agree to pay a “fair price” for the preservative treatments that extend the life of crossties. “I remain confident we can work something out on the pricing front that gets us to market,” said CEO Leroy Ball, “because, as I’ve mentioned before, the alternative is that we will not remain in this business, which I don’t think is good for the industry.” Martin Marietta Materials said in its call that “We’re the largest shipper of stone by rail in the United States, [shipping] almost 2x what our closest competitor will by rail.” CEO Lourenco Goncalves of Cleveland-Cliffs sounded bullish about steel demand, thanks to rising auto production, new solar projects, and the impact of the infrastructure bill, the Inflation Reduction Act, and the CHIPS Act. “What’s happening right now in terms of this resurgence of manufacturing here in the United States is completely underappreciated. We spent the last 25 years convincing ourselves that we could produce everything in China, in India, in Vietnam, in Indonesia, and places like that. Guess what? We can’t. We have to produce here. And I’m glad that this concept is starting to percolate.”

Labor Update

· The latest paid sick leave deal is between BNSF and its locomotive engineer union. The railroad and the BLET agreed to terms that will allow engineers to take paid sick leave without any penalty, while also providing more predictable work schedules. BNSF says the deal will also help recruit and retain employees. In addition, it will help improve workforce morale and translate to more consistent customer service. The deal must still be ratified by BLET members. But based on recent sick leave ratification votes around the industry, that shouldn’t be a big issue. Union Pacific’s 6,000 conductors and trainmen, for example, voted overwhelmingly to approve a new sick leave deal last week.

· More controversial among some Union Pacific workers is the railroad’s recent appointment of Jim Vena as CEO. Several local leaders of the SMART-TD union, which represents conductors, penned a letter to UP’s human resource chief, criticizing Vena’s selection. As reported by Bill Stephens of Trains magazine, the letter (click here to view) alludes to Vena’s job cuts and implementation of Precision Scheduled Railroading while UP’s operations chief prior to the pandemic. The letter was dated July 26th, the day of UP’s announcement. Joanna March of FreightWaves succinctly frames the key question everyone is now asking: “The heart of the matter is whether Vena will focus on improving operations and creating efficiencies or on attracting more business to the railroad and pursuing growth opportunities—even if it means potentially higher costs in the short term via ensuring UP has sufficient employee headcount to ensure smooth operations.”

· Speaking of former operations chiefs, CSX’s Jamie Boychuk will soon hold that distinction. He’ll be leaving CSX, opening the door for CEO Jim Hinrichs to select his own ops chief. Keep in mind that Boychuk worked closely with Jim Vena at Canadian National, prompting speculation that he might wind up at Union Pacific. Note that Norfolk Southern changed its COO after Alan Shaw took office. Same for Canadian National after Tracy Robinson took office.

· The Canadian west coast labor drama appears to be over, this time for real. Workers voted to accept a new contract but not before staging a two-week strike in early July. It will likely take several months for railroads to clear the backlog from the ports of Vancouver and Prince Rupert.

· With the UPS labor dispute now addressed, the next big U.S. negotiation to watch is between Detroit’s Big Three automakers (GM, Ford, and Stellantis) and the UAW union. Their contract expires next month.

BNSF Q2 Earnings

· Lower freight revenues. Higher non-fuel operating costs. That pretty much sums up the second quarter for all six Class I railroads of North America. That includes BNSF, part of Warren Buffett’s Berkshire Hathaway empire. As disclosed in a government filing last week, its Q2 revenues plummeted 12% vs. the same quarter a year ago, the steepest drop among all Class Is. Non-fuel operating costs, meanwhile, jumped 9%, albeit offset by a 35% plunge in fuel costs. All-in operating costs declined 5%. Of course, the decline in fuel costs also meant BNSF collected less fuel surcharge revenue, which is partly why revenues fell so much. But to be clear, its freight volumes were down too—by 11% y/y. The revenue decline, in other words, was hardly just a fuel surcharge issue.

· In the end, BNSF walked away with a 68% Q2 operating margin, highest/worst among the U.S. and Canadian Class Is (see Earnings Scoreboard chart above). It was also five points worse than its own OR in last year’s Q2.

· BNSF divides its rail freight into four broad categories, all of which contributed to that 11% company-wide volume drop. Consumer products dropped 18%, ag products 8%, industrial products 3%, and coal 4%. In revenue rather than volume terms, the declines for these four categories, respectively, were 23% (ouch), 7%, 1%, and 6%.

· The consumer division includes intermodal, shipments for which suffered from the weak market overall—especially for imports arriving at west coast ports like L.A. and Long Beach. But it also suffered from the loss of key customers, most importantly Schneider (which left for UP). In addition, lower spot prices in the trucking market impacted BNSF’s domestic intermodal demand. Mitigating the consumer carnage somewhat was solid growth in automotive volumes.

· For ag products, a key trend was lower grain exports, partially offset by higher volumes of domestic grains, renewable diesel, and feedstocks. Within industrial products, weakness stemmed from lower demand to move chemicals, plastics, lumber, and petroleum products, the latter impacted by refinery outages. And for coal, demand moderated as natural gas prices fell.

· Keep in mind that neither Berkshire nor BNSF itself holds quarterly earnings calls. But just a few notes about its investment plans: The railroad’s biggest project is in Barstow, California, involving infrastructure that will facilitate the flow of goods arriving through the ports of L.A. and Long Beach. A smaller project recently making news is a planned logistics center in Gunter, Texas, north of Dallas-Fort Worth. It would serve as a hub for ag and industrial freight, arriving and departing by rail or transload. The city approved the plan in May. But some local residents are fighting to stop it. A report in the Dallas Morning News recalled: “BNSF’s history with Gunter includes a fatal accident in 2004 when two of its freight trains collided head-on near the city. The crash killed an engineer and four crew members. About 3,000 gallons of diesel fuel were released and caught fire following the derailment of five locomotives and 28 cars.”

· BNSF has a blog on its website called Rail Talk, with various stories and vignettes from around its system. One recent entry discussed its critical presence in Kansas City, which it described as the country’s second busiest rail center behind Chicago. It’s also a crucial midpoint on BNSF’s prized southern transcon route connecting Los Angeles with Chicago. The railroad’s 780-acre Argentine Yard in Kansas City is the largest in its network for merchandise traffic, used for handling and sorting chemicals, plastics, construction products, paper, lumber, food, beverages, and more. Every day, more than 2,100 railcars arrive and depart Argentine Yard, which happens to be a hump yard. There’s a facility to handle intermodal containers and trailers as well. Argentine Yard was originally built by the Atchison, Topeka, and Santa Fe Railway in 1875.

Ferromex Q2 Earnings

· Mexico’s largest railroad Ferromex, partially owned by Union Pacific, posted a 68.5% operating ratio for the April-to-June quarter. As usual, that was higher (in other words, worse) than what its Class I peers in the U.S. and Canada reported. But unlike its peers to the north, Ferromex, improved results versus last year, boosting revenues by 12%, outpacing a mere 3% increase in operating costs. In last year’s second quarter, the railroad’s operating ratio was 74%.

· Ferromex is certainly not immune to the cost inflation prevalent throughout North America. Its Q2 labor costs, for one, spiked by 19% versus a year ago. But revenue trends are strong, consistent with much of the excitement and enthusiasm about nearshoring, i.e., the practice of relocating manufacturing facilities from Asia to Mexico. Mexico’s auto industry is undeniably hot, as CPKC for one gets excited about.

Keep reading with a 7-day free trial

Subscribe to Railroad Weekly to keep reading this post and get 7 days of free access to the full post archives.