Looking Back, Looking Ahead

Railroad Weekly December 16, 2024

courtesy: Steel Wheels Photography

Inside This Issue

· Looking Back: Reviewing the Top Developments of 2024

· Looking Ahead: What’s Coming in 2025?

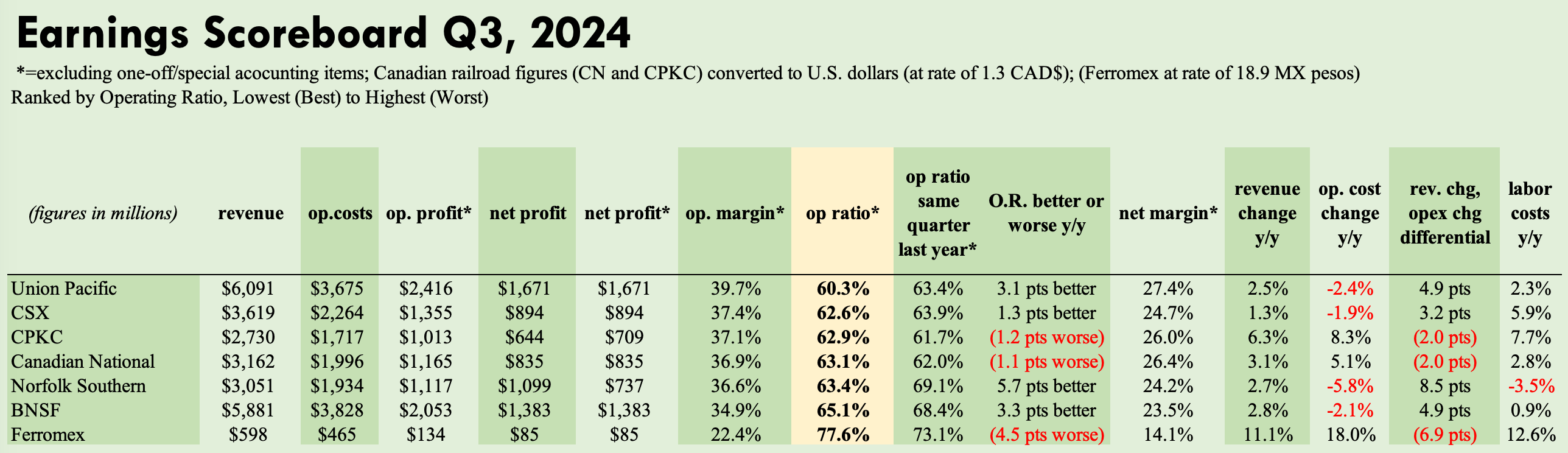

· Cost Curse: Ferromex Sees Margins Fall as Expenses Balloon

· Ferromess: Operations Near Border Muddled by Migrant Crisis

· Dove Affair: Fed Looking Less Likely to Cut Rates in 2025

· Donald Dock: Trump Expresses Support for ILA Union

· Cold Digger: CPKC Mines for Further Gains with Americold

· Happy Holidays! Railroad Weekly Wishes You All The Best in 2025!

Publisher’s Note: As a reminder, Railroad Weekly publishes 48 out of the 52 weeks per year. This is our last issue for 2024. The next issue will be on January 6th.

For a holiday gift idea, please consider my book, American Places. It’s an easy-to-read profile of more than 70 U.S. cities, counties, and towns across the U.S., explaining what drives their economies. It’s designed to provide a greater sense of understanding about how the U.S. economy functions overall, and what makes it strong in some ways and challenged in others. Click on the book image below to buy on Amazon:

Track Talk

“For us, speed is of the essence.”

- Grupo Mexico Transportation CEO Fernando Lopez Guerra Larrea

Looking Back: Railroads in 2024

· It was another eventful year for North America’s freight railroads. The drama ran high at Norfolk Southern, where the investment firm Ancora attempted to topple CEO Alan Shaw. Shaw would retain his job following a nasty proxy war, only to leave the scene after being dismissed for alleged misconduct. Ancora wound up winning some board seats. And as all the dust was settling, NS by year-end was delivering significant improvements in operating ratio. Same for BNSF, which shares Norfolk’s heavy exposure to the mercurial intermodal market. Warren Buffet himself expressed dismay at his railroad’s lagging profit margins. Not long after, the company turned to PSR maven Ed Harris for help, raising some uncertainty among shippers and unions. BNSF downplayed the hire, as its operating ratio indeed got better. Union Pacific has produced the best operating ratio of any Class I for three straight quarters now, capitalizing on its strength in booming markets like Texas. Back in the east, CSX continued to progress in its quest to boost profits, grow volumes, and improve employee relations. Hurricanes were a setback late in the year, and heavy coal exposure remains a vulnerability. But like Union Pacific, CSX held an investor day event this fall that brimmed with optimism. CPKC celebrated its first anniversary since merging, as it worked to harvest revenue and cost synergies. Thanks to these synergies, and thanks to a busy year for hauling commodities like grain and energy, CPKC managed to hold firm to many of its financial goals, even amid macroeconomic weakness, natural disasters, and widespread labor unrest. Canadian National felt the pain more acutely yet still had a good year. Separately, the industry lost two hall-of-fame leaders this year. Jim Foote, CEO of CSX until 2022, passed away in April. He was joined in railroad heaven by Pat Ottensmeyer in July. Ottensmeyer helped orchestrate the CPKC merger as chief of KCS. He also played an instrumental role in developing U.S.-Mexico trade relations.

Top Ten Railroad Trends and Developments of 2024

1. The Industrial Economy, Still Weak: Railroads were hoping for a manufacturing revival following a post-Covid lull. But it wasn’t to be. According to the Institute for Supply Management, the U.S. manufacturing sector contracted every month between April and November. Things in Canada weren’t any better, with Mexico showing some manufacturing gains but hardly yet living up to its greatly-hyped potential. The slump’s causes include higher interest rates, labor shortages, ongoing supply chain pressures, excess inventories, shifting consumer preferences (toward services), and a strong dollar that’s depressing exports. Note also that 2024 was a year in which most commodity prices declined, which is good for consumers (see below) but bad for commodity-heavy economies like Canada’s.

2. The Domestic Intermodal Market, Still Weak: Many are calling it the longest freight recession in memory. For railroads, that’s specifically acute in their domestic container business, where they hotly compete against trucking. Quarter after quarter throughout 2024, domestic intermodal has failed to achieve escape velocity from the long downturn. Occasionally, railroads and their marketing partners (i.e., J.B. Hunt and Hub Group) would speak of some green shoots. But as 2024 nears its end, pricing in the market remains depressed, with truckers getting another second wind from falling fuel prices. The wait for recovery continues.

3. The Consumer Economy, Still Booming: Once upon a time in America, a sickly manufacturing sector meant a sickly economy. Those days are long gone, with manufacturing now accounting for a modest tenth or so of U.S. GDP, depending on how you measure. Healthcare alone is close to 20% of GDP, and this sector saw robust hiring all year. Airlines and hotels were jammed-packed with vacationers. Most generally, consumers spent heartily, never mind higher interest rates (or maybe helped by higher interest rates, considering all the interest income Americans were earning). Unemployment stayed near record lows. Asset values soared (i.e., houses, stocks, cryptocurrencies). Corporate America enjoyed robust profitability, especially in sectors like information technology and finance. Measures of business productivity across the U.S. showed encouraging gains.

4. Railroad Operations Improved: The Covid pandemic was a crisis for railroad operations. In some ways, the recovery from Covid was even worse. Understaffing became a giant problem in 2022 as workers left the industry in droves, just as demand for rail shipments sharply recovered. Not a week went by, it seemed, that the STB

Keep reading with a 7-day free trial

Subscribe to Railroad Weekly to keep reading this post and get 7 days of free access to the full post archives.