Let’s Try This Again

Railroad Weekly May 4, 2026

courtesy: Tyler Sylvest

Inside This Issue

· Let’s Try This Again: UP/NS Resubmit Their Merger App

· New Projections but No Concessions: UP Offering No New Major Carrots

· Who’s to Lose? UP, NS Foresee Grabbing Lots of Biz from BNSF

· Rising Tide But Not Satisfied: BN Improves O.R. But Eyes Even Better

· And to America’s North? Canada’s Rail Margins Go South

· Zeal for a Deal? CN Hints It Might Back UP/NS If Concessions Surrendered

· A Deal With UP? No Way, Says CP

· Not All Lose from Bad News: For RRs, Iran War Opens New Opportunities

· Trinity’s New Reality: A Rail Economy That’s Improving

Track Talk

“Enough is enough. We’ve had enough consolidation.”

-CPKC CEO Keith Creel

The Latest

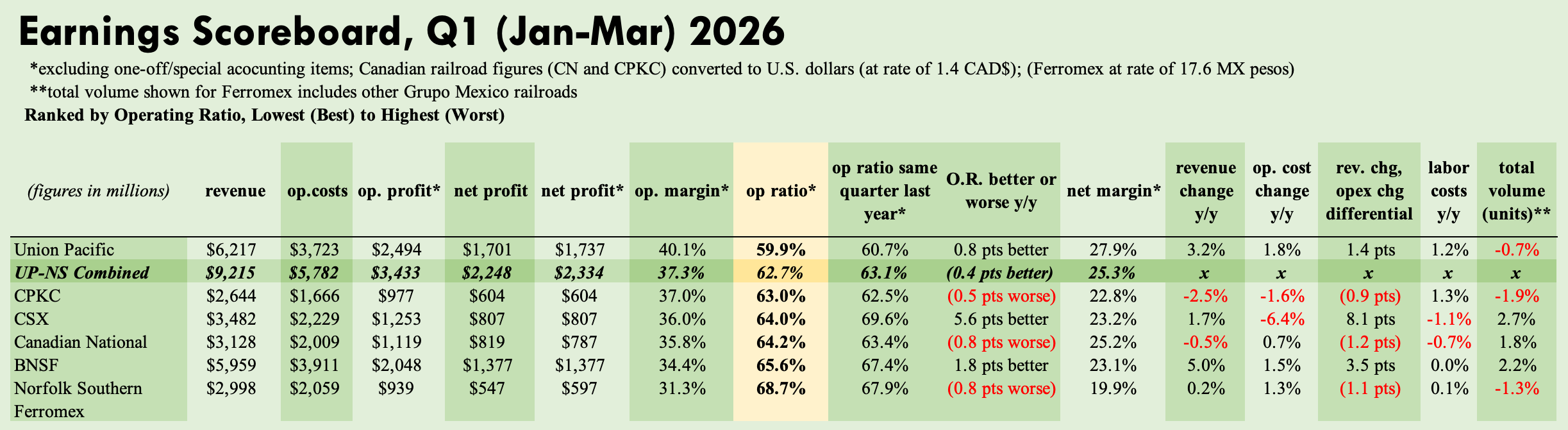

· Hey, hey, it’s already May. Q1 railroad earnings season is now all but finished, with just Ferromex still to report. BNSF, Canadian National, and CPKC all reported last week, expressing familiar concerns about headwinds like tariffs and the housing slump, but also emerging areas of optimism about manufacturing activity, intermodal market share gains, and moving more North American commodities now in short supply globally. But of course, the most anticipated development last week was Union Pacific’s re-filing of its STB application to buy Norfolk Southern.

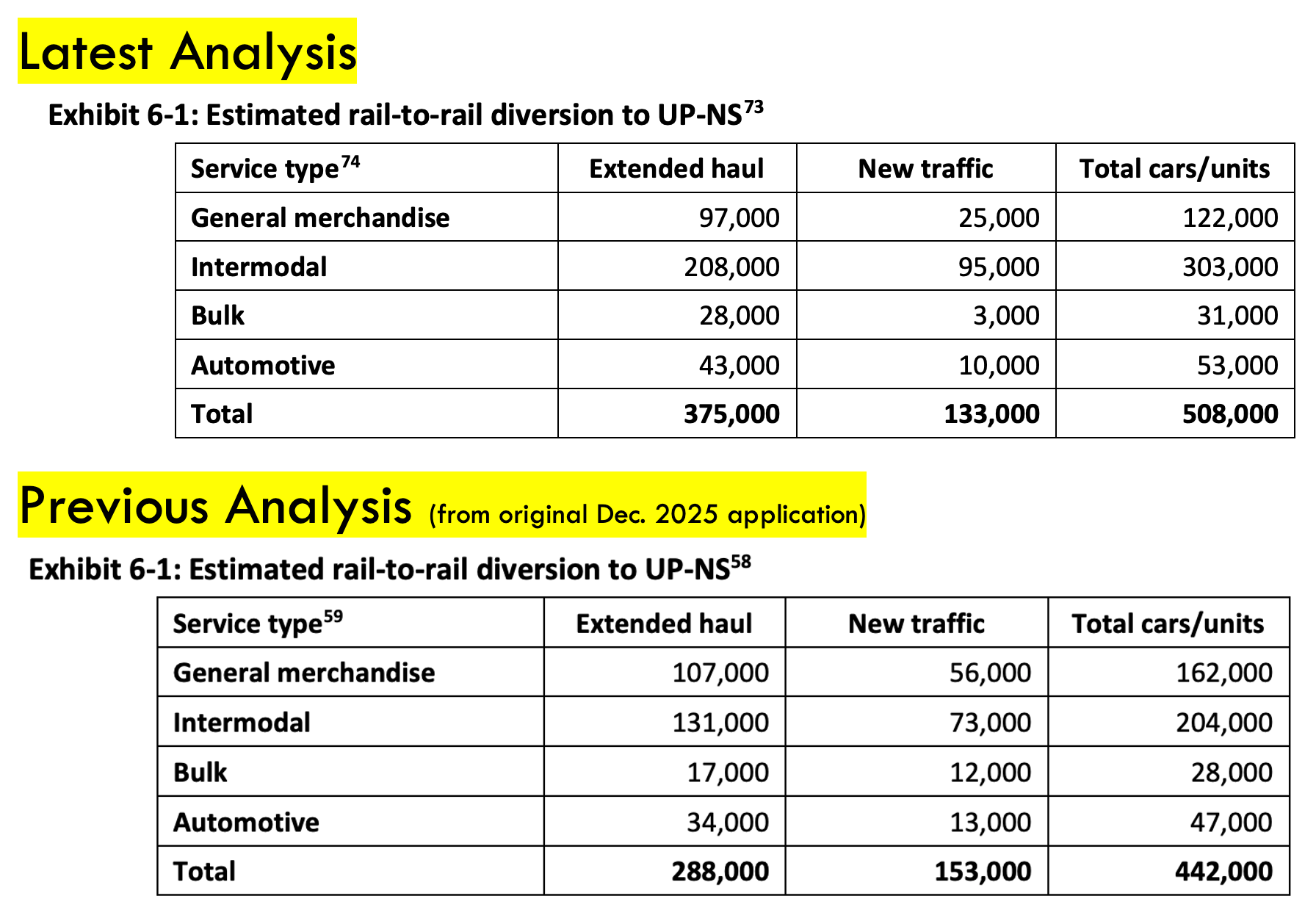

· The revised document—more than 7k pages—provides more detailed data about traffic projections, as the STB and other railroads demanded. In fact, its new figures show “more opportunities to attract traffic than initially anticipated.” It now expects to capture more than 2.1m carloads a year worth of freight from the highways—it previously said more than 2m. It also sees the merger creating 1,230 new jobs, up from 900 projected in its earlier application.

source: UP-NS merger applications

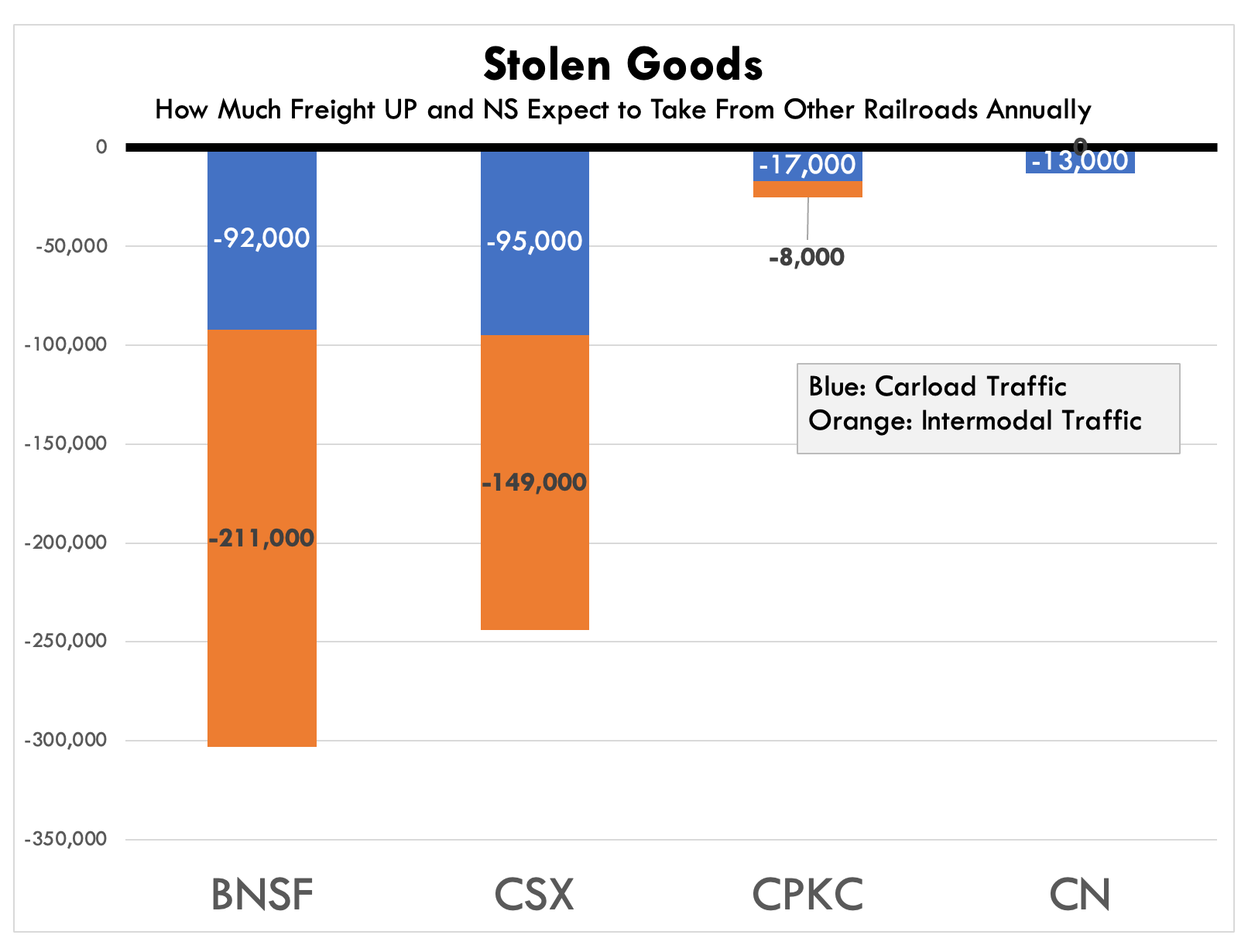

· The new document features an updated assessment of how much traffic UP and NS expect to grab from other railroads. They now see annual gains of 508k carloads and containers, versus 442k previously (they’re now more bullish on intermodal, bulk, and autos). They also said 74% of this expected market share gain is currently moving as interline traffic; in other words, UP or NS currently moves it jointly with other railroads (its previous estimate here was 66%). BNSF clearly stands to lose the most, as this chart shows:

source: revised UP-NS merger application

· The new application addressed some minor concerns, like worries about the combined railroad’s control of a switching railroad in St. Louis. But for anyone expecting major new concessions… crickets. UP’s chief Jim Vena has argued stridently that the transaction as is will bring big benefits to a wide array of stakeholders.

· Not so, says a new coalition of merger opponents. The “Stop the Rail Merger Coalition” says flat out: “The UP-NS Merger is a Bad Deal for America.” Members include BNSF and CPKC, but not CSX nor Canadian National. As discussed below, CN appears amenable to a deal if UP is willing to surrender enough valuable concessions. Other members of the new group include the Teamsters union and trade associations representing chemical and ag shippers.

· The STB will now review the revised application. If this one meets its criteria for approval, the real debate will begin. In-person hearings could happen this summer, where parties both for and against can argue their case. Assuming no direct interference from President Trump or anyone else, the merger’s fate will hinge on the opinions of STB chair Patrick Fuchs and his fellow board members Michelle Shultz, Karen Hedlund, and potentially Richard Kloster, assuming his nomination is approved. There’s a fifth board seat also currently vacant.

Other Developments

· Trinity, which builds and leases railcars, sounded cheerful in declaring: “The rail economy is improving.” It cited U.S. industrial production growth of 2.4% last quarter, consistent with a more bullish manufacturing PMI (that’s the closely-followed report that surveys purchasing executives). Trinity itself is seeing a pickup in customer inquiries. Railcars in storage, meanwhile, dropped below the 20% mark, a sign of declining railcar supply and rising rail freight demand. But the company warned: “The picture isn’t all clean.” Inflation is still elevated, and employment has flattened. That continues to weigh on consumer-driven markets, particularly autos and intermodal; and tariff uncertainty remains. “But the direction is the right one, and we’re positioned for it.” Trinity produces roughly 30% to 40% all new railcars, the market for which shrank markedly last year. It’s expected to be depressed again this year (about 25k new deliveries based on industry forecasts). But for railcar makers, this might be demand delayed but ultimately not denied.

· Caterpillar, which owns the locomotive maker Progress Rail, said in its latest earnings call that “rail services and locomotive deliveries are both anticipated to grow for the year.” It didn’t say much else about rail developments, specifically. But Caterpillar did note how its various business lines are benefiting from the big data center boom, and Corporate America’s capital spending boom more generally. “That has translated to accelerated order rates for us.” The company says it’s providing “the critical minerals, the reliable power, and physical infrastructure that the modern world depends on.” Less happily, it expects to pay as much as $2.4b in tariffs this year. Yikes.

Q1 Earnings

BNSF

· It’s a new era for Berkshire Hathaway, with the legendary Warren Buffett now retired as chief executive. His successor, Greg Abel, led his first annual shareholders meeting this weekend, providing updates on the company’s many businesses and many business investments. It’s both a major shareholder in blue-chip American firms

Keep reading with a 7-day free trial

Subscribe to Railroad Weekly to keep reading this post and get 7 days of free access to the full post archives.