Inside This Issue

· Creel of Fortune: CPKC Thriving… But Labor Doom Looms

· Same Song on the Ratio: BNSF’s Q2 O.R. Identical to Last Year’s

· Mexual Healing: US Ag Shippers Demand Better from Ferromex

· Good Streak But Far From Peak: IM Biz Growing But Still Down from Past Highs

· Bama Mia! NS Announces Big Investment in Alabama

· Market Malaise: Weak U.S. Economic Data Point to Rate Cuts Next Month

· Coming Monday: CSX Will Be Last of the Class Is to Report for Q2

· In Memoriam: Rail Industry Mourns the Passing of Pat Ottensmeyer

Track Talk

“Pat’s vision and leadership played a monumental role in the great history of Kansas City Southern. He helped reshape the railway industry. We’ve lost a truly remarkable leader and a cherished friend.”

-CPKC CEO Keith Creel, paying respects to the late Pat Ottensmeyer

The Latest

· July is now finished, and North American rail traffic continues to show y/y growth. Modest growth, yes. But growth nonetheless. So far in 2024 (data is available through July 27th), carload volumes according to AAR are up 2% y/y. Give most of the credit to a revival in intermodal activity, which is up 8%. But remember, at this time last year, intermodal volumes were running 10% below 2022 levels. There’s a long way to go before railroads achieve the sort of growth they seek—growth to levels above and beyond their peak six years ago.

· North American carload traffic, meanwhile, (which excludes intermodal) is down 3% year-to-date. The principal reason is coal’s 15% y/y plunge. But exclude coal as well and still, the industry is growing just fractionally this year (volumes up 0.3%). Carriers have talked about other areas of softness like forestry products and certain construction materials. North America’s industrial output remains weak. So does new housing construction. Labor unrest is a recurring concern, most recently in Canada and along America’s eastern and Gulf coast ports. There are in fact just three broad AAR categories of non-intermodal freight that are up more than 1% in volumes across the continent so far this year—one is chemical freight, another is petroleum, and the third is grain.

· The Intermodal Association of North America (IANA) gave some more detailed data about demand in just the April-to-June quarter. It said total volumes were up 8% y/y (see chart).

· With August now here, it’s time for Canada’s Big Two railroads to prepare for the autumn grain harvest, which is looking like it will be a big one this year. Both CN and CPKC published their annual Grain Plans last week, describing, for example, the challenges they expect to face. CN for its part expressed concerns about a worker shortage caused by new federal labor regulations. The railroads are also frustrated by Vancouver port’s inability to load grain during rainy weather. As CPKC grumbles, “Unlike Vancouver facilities, other Canadian export terminals and U.S. Pacific Northwest (“PNW”) terminals safely load grain onto vessels during periods of rain, avoiding capacity losses.” Of course, the biggest issue of all for both carriers is a looming Teamsters strike—the union represents engineers and conductors. (Read more in the CPKC earnings review below).

Summary of Canada’s top ag/livestock products by province (source: Government of Canada):

· A few updates from Norfolk Southern: The railroad last week announced a $200m growth and investment plan for its 3B corridor in Alabama, which links northern and central parts of the state with the port of Mobile on the Gulf coast. It’s another manifestation of the rapid industrial expansion underway through the U.S. southeast. Less happily for NS, the U.S. Justice Department sued it last week, alleging failure to give dispatching priority to Amtrak, which U.S. law requires. Separately, NS CEO Alan Shaw was a guest on David Novak’s “How Leaders Lead” podcast, in which he recounts the highlights and lowlights of his eventful tenure, and what he’s excited about for the months and years to come.

· Less than four months after the passing of former CSX chief Jim Foote, the railroad universe lost another one of its grand figures. Pat Ottensmeyer, Kansas City Southern’s former chief, passed away last week. Ottensmeyer became a critical figure in the industry’s fortunes, first by championing U.S.-Mexico trade and later by orchestrating KCS’s sale to Canadian Pacific.

The Economy

· There was lots of red on the market chart last week: Stock prices were down, oil prices were down, borrowing rates for homebuyers and the U.S. government were down… In addition, the ISM survey index of manufacturers was down. Job growth in July was down. One thing that didn’t go down was the Fed’s targeted interest rate for overnight borrowing. Chair Powell and friends kept rates steady as expected last week. But they also telegraphed a possible rate cut to come at its next meeting in September. The weaker jobs data, published two days after the Fed’s Wednesday announcement, makes a September cut even more likely. The question is now becoming: Will the cut be not just a quarter point but a full half point?

· More specifically about the July employment report, it certainly wasn’t terrible. The economy still created 114k new jobs during the month. But this was below the average monthly gain of 215k over the prior 12 months. The unemployment rate ticked up to 4.3%, still historically low but up from just 3.5% a year earlier. Once again, the giant healthcare/social services sector led the way, accounting for almost two-thirds of all the new jobs. Construction was another area of growth, with lots of new jobs for specialty contractors working on non-residential projects. Warehouse and courier jobs were up a lot too. Ditto for jobs at restaurants and bars. But information-related jobs declined sharply (i.e., in telecom and publishing). The finance and professional service sectors showed losses. Manufacturing was more or less flat. Rail transport jobs were down a bit.

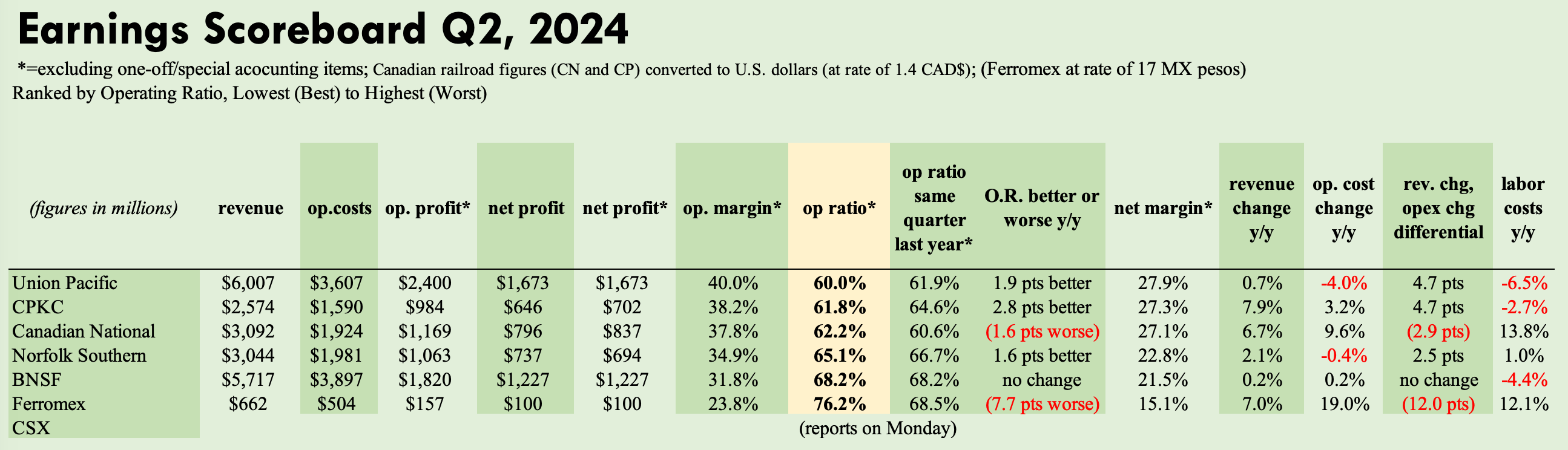

Q2 Earnings: CPKC

· Before anything else, CPKC’s chief Keith Creel paid respects to the late Pat Ottensmeyer, his counterpart at Kansas City Southern during their merger negotiations. The two executives would create the combined Canadian Pacific-KCS, or CPKC, in a deal finalized last spring. Now more than one year old, the enlarged railroad is performing well and delivering on promised merger synergies. Creel affirmed that “Pat’s legacy lives on. It can be seen in the work we do every day at CPKC.”

· He’s not exaggerating. CPKC, despite the many well-documented challenges facing the rail sector, is faring well in 2024. In Creel’s own words, “I’m extremely pleased with the first half of the year [and] even more excited about what the second half holds.” Last quarter (April to June), the railroad brought its operating ratio down below 62%, a nearly three-point y/y improvement. That wasn’t easy given a 3% y/y increase in operating costs. But impressively, revenues jumped 8%. In fairness, some of this increase was a mere recovery from last year’s Canadian port strike on the west coast. But there were lots of other reasons for the gain, for example, grain.

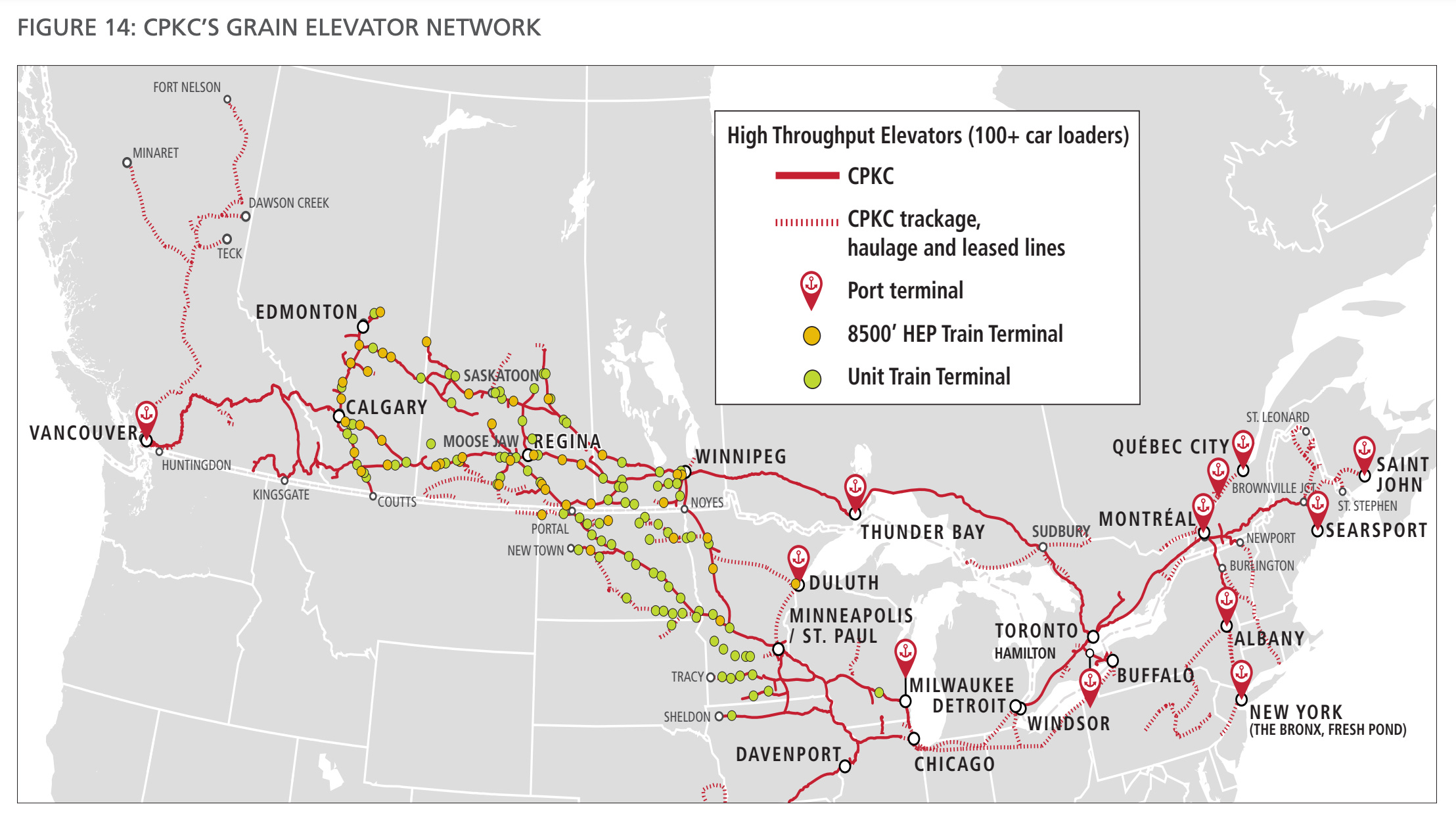

· Of all the Class I carriers across the continent, CPKC is most exposed to bulk traffic, including agricultural products and more specifically grain (wheat, corn, canola, soybeans, etc.). Revenue from grain last quarter rose 17%, thanks in Canada to a “stronger-than-expected spring and summer sales program” as farmers “reduced their on-farm inventory in preparation of the upcoming harvest.” CPKC’s U.S. grain franchise, meanwhile, was boosted by demand for corn shipments to the Pacific Northwest, Mexico, and Alberta, along with wheat shipments to Mexico. One major benefit of bringing CP and KCS together was creating the ability to seamlessly move grain output from areas like southern Canada, North Dakota, and Minnesota into Mexico. Sure enough, said marketing chief John Brooks, “we’ve really seen here this summer, our grain shipments down into Mexico accelerate.”

· CPKC combines energy and chemicals as a single entity for reporting purposes. But if they were separate, grain would be the railroad’s single largest revenue generator, larger even than its intermodal business. To put a figure on that, a full 18% of its revenue came from grain last quarter. Encouragingly, the new grain crop this fall looks promising. “Early indications are that this harvest will be more in line with our five-year average, or if not, stronger. That, coupled with our regulated grain pricing of approximately 6.5%, has us well positioned in Canadian grain.” Executives also assured that the railroad will have the capacity ready to handle what comes, even in congested western Canada. Recall that last autumn, demand to move grain was far below normal (about 25% below CPKC’s available train capacity for the full season). And that alone should make it easier for CPKC to show y/y volume and revenue growth this year.

· Separate from its earnings report last week, CPKC also published its grain outlook for the 2024/25 season. It notes: “On June 20, 2024, Agriculture and Agri-Food Canada (AAFC) estimated the total size of the upcoming crop to be 94.4 million metric tonnes (MMT), with a crop in Western Canada of approximately 71 MMT. Our grain customers currently estimate Western Canadian crop yields at a higher level than AAFC, with most customer estimates now in the high 70 MMT range.”

CPKC’s grain network and recent grain volume performance (source: company reports):

· As for other lines of business, potash revenues also benefitted from favorable y/y comparisons, with a Portland shipping facility offline last spring. Currently, the “potash supply chain is performing very well and export demand is sold out for the second half of the year. We are on pace to set a record all-time tonnage with Canpotex this year.” Canpotex, based in Saskatchewan, is the world’s largest potash exporter. Coal revenues managed to grow despite a volume decline, helped by Canadian coal moved to Vancouver and Thunder Bay for export (coal was just 7% of total revenues).

· CPKC’s critical energy/chemicals/plastics franchise was strong, growing both revenues and volumes by double digits y/y. Merger synergies are leading to more movements of liquified petroleum gas, plastics, renewable diesel, and refined fuels, for example. “We are connecting markets from Alberta to the Gulf Coast and into Mexico with our single-line haul service.” Here again, the merger synergies are evident.

· The auto sector was strong too, showing exceptionally strong y/y growth, a testament to the “closed-loop” service CPKC can now offer up and down the continent. Yes, another merger synergy. The railroad also opened a new Dallas auto compound in June. “This compound is part of our playbook that unlocks an entirely new supply chain model for the OEMs [original equipment manufacturers like GM and Ford], giving them new competition, service, and capacity certainty like they’ve never had before.” Brooks added that auto synergies from the merger are materializing faster and earlier than expected.

CPKC Market Trends:

· Less healthy were markets like forestry, steel, and frac sand. The domestic intermodal market likewise remains tough, albeit with promising growth opportunities. CPKC’s cross-border MMX service (considered part of its domestic intermodal entity), has been well-received but still running with suboptimal levels of demand, meaning suboptimal train lengths. Operations in Mexico are improving (they were tough a year ago) and cross-border fluidity will improve with a new bridge opening at the Laredo crossing. Looking ahead, it sees a “strong pipeline of opportunities stacked up to the back half of the year,” from both wholesale and retail shippers. It’s also poised to establish a new Alabama interchange with CSX for shipments between Mexico and the U.S. southeast. On the international intermodal side, executives are still bullish on Mexico’s Lazaro Cardenas port, which could benefit from an east coast U.S. port strike this fall. But speaking of strikes…

· We’ve gone this far without mentioning the elephant in the room: A looming Teamsters strike that might shut both of Canada’s big freight railroads down. The threat alone is already causing CPKC to lose port traffic, with a work stoppage possibly starting later this month. August 9th is a key date—it’s when a government labor board will rule on essential services that might be mandated in the event of a strike or lockout. Creel, alas, said CPKC is still “far apart” with the Teamsters on reaching a compromise. “I’m just being transparent and honest. It’s going to be a challenge. We’ve offered to enter binding arbitration, given we understand the potential damage to the Canadian economy. We understand the damage and the pain and suffering on our employees, even those that might be out on strike as well as those that aren’t out on strike. It's not a good outcome for anyone.” But, he added, “we’re not going to do a bad deal either. I’m not going to punish this company or let this company suffer because we don’t have the discipline to say no and do what’s in the best long-term interest for all employees.”

· Creel says candidly: “It’s most probable that we’ll have the work stoppage [at] both railroads.” This utterance alone helps explain why CPKC’s stock dropped 4% last week, despite its otherwise strong results and bullish outlook.

Dueling Quotes: Statements from CPKC (left) and Canada’s Teamsters Rail Union (right):

· As it nervously awaits the government’s labor ruling, and the potential strike that would damage Q3 margins, management is optimistic about Q4. Pricing momentum remains strong. The network is operating fluidly. Merger synergies continue to build. The autumn grain harvest is looking good. Cost inflation is moderating. “I think in Q4,” said CFO Nadeem Velani, “we’re set up to have a record operating ratio for CPKC, and I think it’s going to be a very strong finish to the year.

· In summary, Brooks concluded, “The volumes in the first half came in slightly better than we expected, and we’re off to a strong start in Q3. While the macro remains challenging in some areas, overall demand has stabilized and more importantly, we continue to have line of sight [with] strong differentiated growth from synergies and self-help initiatives and disciplined pricing. The operations team is delivering reliable, resilient service to our customers, and my team is laser-focused on selling into that service and taking advantage of our expansive new network. I’m excited about what we’ve accomplished so far this year and even more for the opportunities we have ahead of us” But he also cautioned: “We got to get through what is likely going to be a strike that brings a certain level of uncertainty. Of course, we’ve got an election year [and] we’ve got a macro environment that is still not great in some areas.” And as Creel mentioned, “the freight environment continues to be challenging.”

Q2 Earnings: BNSF

· Berkshire Hathaway, the parent company of BNSF, also reported its Q2 results. It

Keep reading with a 7-day free trial

Subscribe to Railroad Weekly to keep reading this post and get 7 days of free access to the full post archives.