Inside This Issue

· Margin Drops on Sloppy Ops: UP and CSX Report Their Q2 Earnings

· More Demand Than We Can Handle: An Emerging Q2 Theme

· A Coming Recession? Railroads Don’t Seem Too Worried

· Border Transporter: KCS Gets Good News from Mexico

· The CP-KCS Merger: STB Sets Hearings for September

· Intermodal Matters: Updates from J.B. Hunt and Knight-Swift

· Southern Hospitality: NS Raises Pay for New Hires

Track Talk

“I think that collectively, us and our rail providers all understand that there’s additional demand, additional revenue, additional volume waiting on us to improve our service… I do anticipate that we’re going to see some improvements during the second half of the year. The key question is when.”

- J.B. Hunt intermodal President Darren Field

The Latest

· Second quarter earnings season is now underway, with Union Pacific and CSX both reporting strong profits… but not as strong as in the same quarter last year. Operating ratios fattened by a good five to six percentage points, owing to higher fuel prices and most importantly, poor operational performance blamed on staffing shortages. With industry margins structurally so high, financial pressure to improve fluidity isn’t terribly intense. But the STB and most importantly shippers are up in arms, understandably given the stakes. Last week, NPR’s Marketplace featured a story about the dismal railroad situation, noting how delays have cost the grain industry—according to Max Fisher of the National Grain and Feed Association—more than $100m in this year’s first quarter alone. The NPR piece, as an aside, called freight trains the “bloodstream of the economy, circulating products throughout the country.”

· A separate report by Barron’s mentioned how railroads are often called the “canary in the coal mine for the U.S. economy because they carry roughly 40% of the country’s long-distance freight.” The Barron’s piece (actually a podcast which you can access here:) https://podcasts.google.com/feed/aHR0cHM6Ly92aWRlby1hcGkuYmFycm9ucy5jb20vcG9kY2FzdC9yc3MvYmFycm9ucy9zdHJlZXR3aXNl/episode/NzNkMzYxMmMtMGEwZi0xMWVkLWFhZTQtZmY5YTcxMmNjZGQ0?sa=X&ved=0CAUQkfYCahcKEwjIp4eDrI_5AhUAAAAAHQAAAAAQEQ&hl=en )

noted how the Class I railroads cut 29% of their workers over the past six years, as part of their adoption of Precision Scheduled Railroading (PSR). Prior to PSR, railroads operated what Barron’s described as a hub-and-spoke system, where trains left when they were full, and stopped at yards so they can be switched around so that each train carried similar goods. With PSR, advanced most famously by Hunter Harrison, freight railroads began behaving more like passenger railroads, moving trains at scheduled times from point to point, with mixed goods and limited car switching. The result: Running longer trains with many fewer workers. But PSR is under attack in some circles now, not just among unions but also those dismayed by the railroad industry’s loss of market share to trucks during the pandemic. Some are also asking whether PSR might have been more appropriate for Canada’s railroads (where distances are longer and thermal coal dependence is less) than for U.S. railroads. In producing the story, Barron’s spoke with Citi analyst Chris Weatherbee and Rachel Primak of FreightWaves.

· Kansas City Southern—and by extension Canadian Pacific—received welcome news from south of the U.S. border. Mexico’s government agreed to extend KCS’s exclusive rights to operate its Mexican rail franchise for another ten years. Its exclusivity will now run until 2037. In exchange, KCS agreed to invest up to $200m in developing rail infrastructure in the state of Guanajuato north of Mexico City. KCS first invested in Mexico’s largest railroad during the mid-1990s before buying a controlling ownership stake in 2005.

· Separately, CP and KCS won another influential supporter for their merger. Archer Daniels Midland, a large agricultural commodity trader based in Chicago, dismissed concerns that the combined railroad might force shippers using its Mexican rails to also use its rails north of the border. ADM moves a lot of commodities from the U.S. to Mexico, sometimes using multiple railroads with an interchange to KCS Mexico at the border. Archer Daniels Midland is one of the so-called ABCD companies (along with Bunge, Cargill, and Dreyfus) that dominate agriculture commodity trading globally. They feature prominently in this recently published book: https://www.amazon.com/World-Sale-Javier-Blas/dp/0190078952

· Mark your calendars for September 28th, 29th, and 30th. The STB announced hearings on the CP-KCS merger will be held in Washington on those three days. The hearings, the STB said, “will allow the Board Members to directly question the Applicants and other interested persons about the issues that have been raised.”

· Extreme heat across North America and elsewhere gave a reminder of threats posed by climate change—threats to railroad operations specifically, and to human health and economic growth more generally. Union Pacific, for one, has said repeatedly that climate change is a major risk to its business.

· There are limits to what railroads can do as far as raise pay for workers, absent a formal agreement with unions. But Norfolk Southern last week said it would increase conductor trainee pay to $25 per hour, among other sweeteners. In addition, conductor trainees in priority locations can earn up to $5,000 in starting bonuses. These locations include Cincinnati, Harrisburg, and Louisville. NS says a first-year conductor earns an average income of $67,000, which grows over time with seniority. They also get health insurance, pension benefits, and a 401(k) savings option. “Conductor trainees should expect to complete a training program of approximately 16 weeks before promoting to a conductor position. The first three weeks of training occur at the Norfolk Southern Training Center in McDonough, Georgia. The remaining weeks of training take place at or near their hiring location.”

· A few other developments from across the rail industry: The Presidential emergency board began its work this weekend, with non-binding recommendations expected in mid-August. Oakland’s port was disrupted, not for anything to do with the contract dispute between dock workers and shipping firms—the issue was a trucker strike related to a new California law pertaining to self-employed workers. In Wisconsin, railroad stakeholders gathered for an event hosted by the Midwest Association of Rail Shippers (MARS). Jim Foote of CSX, Eric Gehringer of UP and Patrick Fuchs of the STB were among the speakers. Also presenting was the consulting firm PLG, which made this interesting point: Chemicals now account for 14% of all non-intermodal rail traffic, second only to coal. PLG also discussed the potential for railroads to gain from North America’s transition to cleaner energy—greater demand to move minerals used in batteries, for example. This week will be another busy one: Earnings from Canadian National, Canadian Pacific, and Norfolk Southern, plus another Federal Reserve announcement on interest rates.

Q2 Earnings: Union Pacific

· “There’s more to be done, but we’re moving in the right direction.” So said UP’s CEO Lance Fritz, hopeful of convincing shippers, investors, and regulators that the worst of its operational woes are close to over. Freight car velocity, a good measure of how efficiently a railroad is moving freight, rose from a lowly 180 daily miles per car in April to 188 in May and 192 in June. That’s progress. But it’s still short of the 213 UP averaged during last year’s second quarter.

· By now you know the familiar refrain: It’s a shortage of labor, UP and its rivals say, that’s chiefly responsible for the difficulties. It’s absolutely not, they insist, related to the adoption of Precision Scheduled Railroading (PSR). “Let me start first by saying emphatically that PSR is not the cause of our problems in the second quarter,” Fritz asserted during the company’s earnings call. He said PSR has in fact helped address many inefficiencies, like too many unit trains full of commodities and workers “touching cars more than we needed to.” Yes, UP cut its workforce significantly. But it also sharply cut the number of trains it runs, and the number of locomotives it deploys.

· Plenty of workers, shippers, politicians, and regulators will disagree, arguing that railroads—in accordance with PSR or whatever reason—cut staff far too zealously both before the pandemic and in response to it. One thing nobody can argue, however, is the positive impact PSR has had on railroad profits. For all the headbanging about railroad operational distress this spring, UP produced another set of financial results that would turn most corporations green with envy. Its operating ratio, however, worsened by about five full percentage points y/y. Still, at 60%, that’s hardly an O.R. worthy of shame. The bottom line is that UP like other railroads have more demand than its faulty operations can handle right now, leading to strong pricing power. That includes the power to levy surcharges to offset a surge in diesel fuel prices—albeit with a time lag that did result in margin-hurting fuel inflation last quarter (fuel prices have started to decline in recent weeks). Also helping to offset the drag from fuel and poor operations was a more profitable mix of traffic. Or put another way, higher-margin freight like coal accounted for a larger percentage of its overall haulage.

· Labor costs are poised to rise substantially as stalled contract talks with industry unions near a resolution. That will mean a five-year deal backdated to 2020 and running through 2024. Speaking with Yahoo Finance last week, Fritz said the industry is seeking “reasonable wage increases,” changes to the “Cadillac” health care plans currently offered, and modernization of work rules. Fritz doesn’t expect a work stoppage, even if both sides can’t agree on a deal after the Presidential Emergency Board makes its recommendations. The most likely next step would instead be Congress imposing the PEB’s recommended terms. Here’s the link to the Fritz interview: https://news.yahoo.com/union-pacific-ceo-on-labor-negotiations-pretty-far-apart-right-now-175113622.html

· Demand last quarter remained strong for UP, with revenue jumping by double-digits y/y for coal, chemicals, metals/minerals, forest products, intermodal freight, and especially autos/auto parts. The latter saw a 31% revenue improvement as vehicle production recovered (partially) from the severe semicon shortage. To be clear, much of this revenue growth was thanks to pricing, not volumes. Only for metals/minerals and autos did carload volumes rise by double digits. In the case of intermodal, volumes declined 8%, even as revenues rose 15% (talk about strong pricing power!). The international intermodal market, alas, still suffers from bottlenecks preventing the supply chain from meeting demand. Domestic intermodal is healthier.

· One reason for coal’s big 16% y/y revenue spike (despite a mere 2% increase in carloads): Two new contracts that UP managed to win. More generally, the market remains strong as high natural gas prices incentivize more coal usage by power plants—power plants now striving to meet electricity demand amid extreme heat throughout much of the U.S. Elsewhere in UP’s bulk business, grain and fertilizer shipments were down. But biofuel shipments were up.

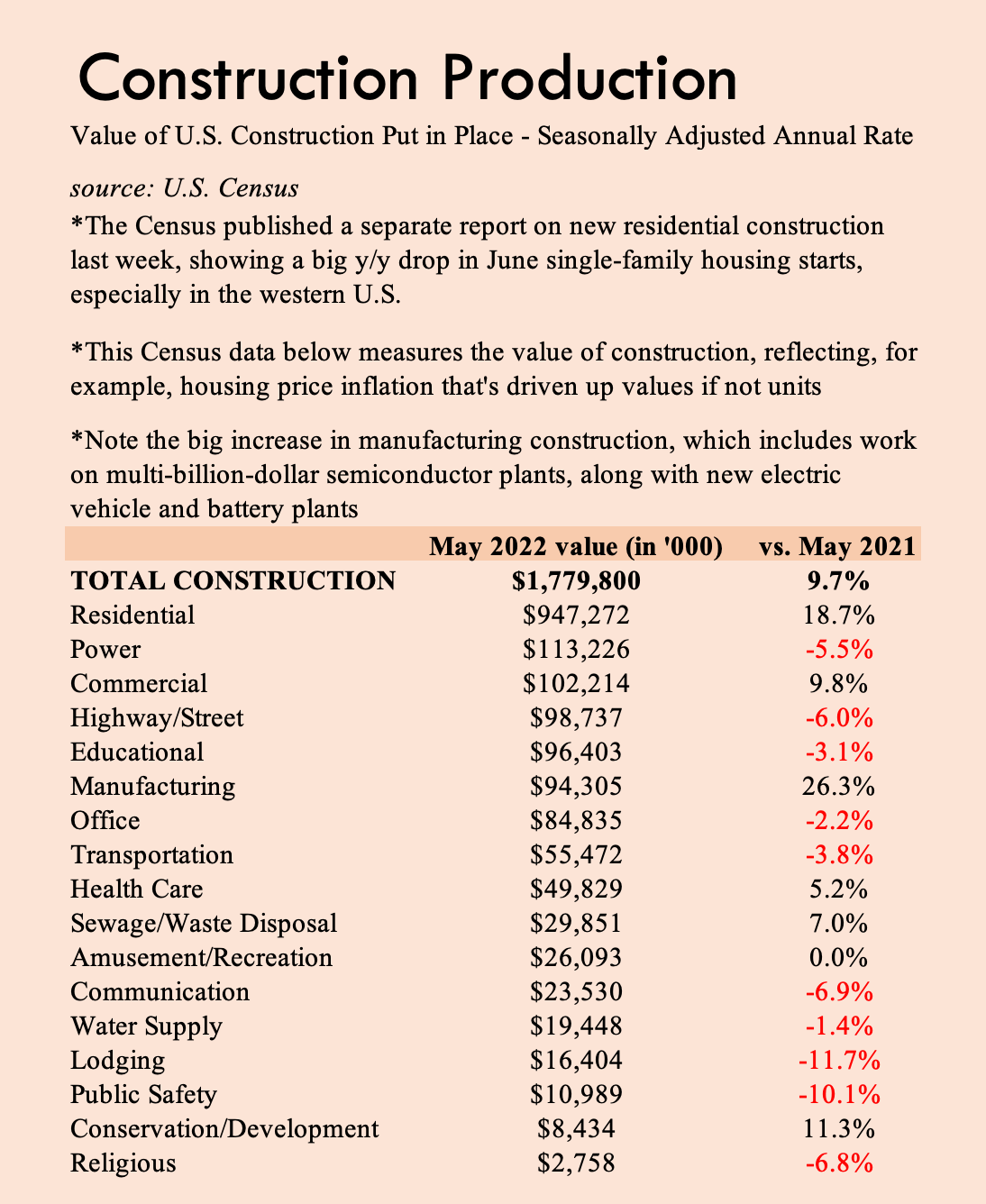

· With respect to industrial demand, this is where UP feels it’s leaving a lot of business on the table, especially as it prioritizes bulk traffic (at times on orders from the STB, as with shipments to Foster Poultry Farms in California). The railroad simply can’t move as much as customers want it to move because of low network velocity linked to labor shortages. The demand is certainly there though, never mind talk of a slowing economy. That’s even true for forest products, never mind the unmistakable slowdown in single-family housing starts. Construction more broadly, however, remains strong, driving demand to move metals and minerals, including frac sand for energy companies. The latest Census report on U.S. construction spending (for May) shows big y/y gains in the value of even residential construction, and especially for construction of manufacturing facilities.

· What about auto demand? Will it continue to recover? Yes, UP believes. Semicon availability is improving, and extremely low inventories mean dealers need to be restocked. Some automakers

Keep reading with a 7-day free trial

Subscribe to Railroad Weekly to keep reading this post and get 7 days of free access to the full post archives.