Inside This Issue

· Returning Ghosts: Labor Threats Loom Again

· Tis the Season: Q2 Earnings Start Now

· Cross-Border Battles: Rail Competition in the U.S.-Mexico Market

· Maritime Matters: Key Developments at Sea

· Looking Back: Hunter Harrison, Shortly Before His Passing

Track Talk

“Railroaders do not feel valued. They resent the fact that management holds no regard for their quality of life, illustrated by their stubborn reluctance to provide a higher quantity of paid time off, especially for sickness. The result of this vote indicates that there is a lot of work to do to establish goodwill and improve the morale that has been broken by the railroads’ executives and Wall Street hedge fund managers.”

-Statement from the BMWED-IBT union, following the failure of its members to ratify the new national work contract

Latest News

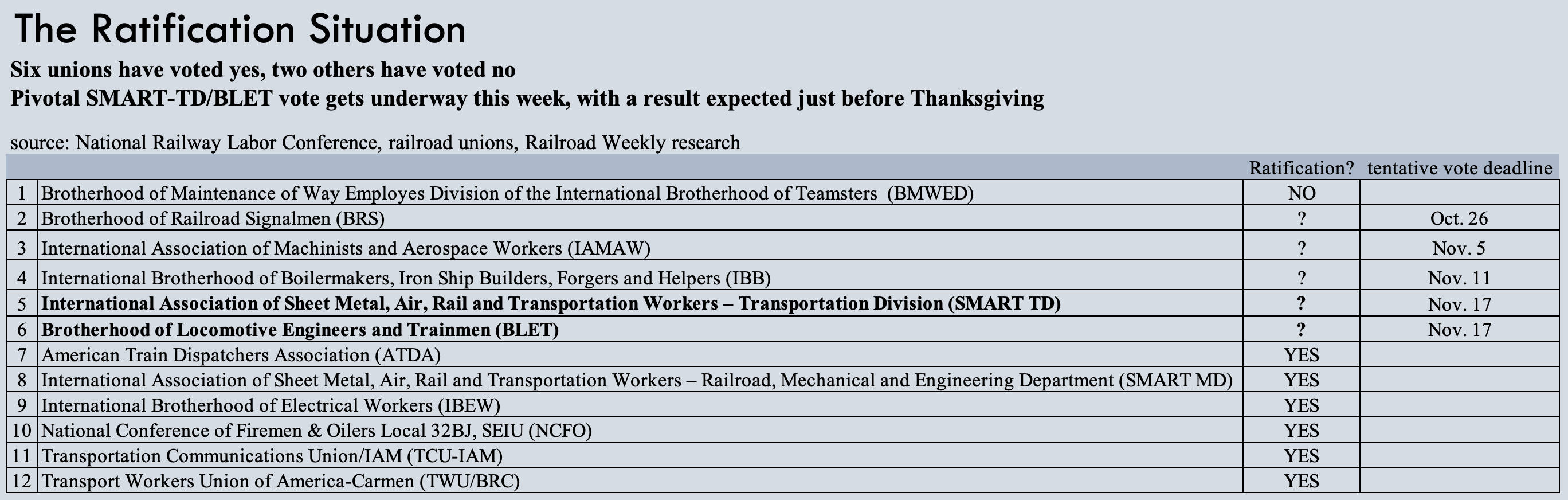

· A familiar ghost is haunting once again. Fears of a railroad labor strike are back, causing new nightmares as Halloween approaches. A month ago, everyone breathed a sigh of relief when railroads and their unions—with help from Washington—reached an 11th-hour contract deal to avert an economically catastrophic work stoppage. But the deal was only tentative, requiring ratification by union members. Of the 12 unions involved, half have now indeed voted to ratify. But another—the BMWED union—announced last week that its members voted no, by a roughly 56% to 44% margin (on 11,845 submitted ballots). What does this mean? Nothing yet (see labor update below). But five additional unions have yet to complete their voting, including the industry’s two largest unions, the BLET and SMART-TD. Their voting will in fact start this week and run for about a month, ending a week before Thanksgiving. If they vote yes, the BMWED’s rejection will carry less weight. But if one or both vote no? The prospect of economic Armageddon returns, likely triggering a Congressional response.

· The industry’s renewed labor anxiety comes just as third quarter earnings season gets underway. Union Pacific and CSX open the festivities on Thursday of this week. Norfolk Southern and the two Canadian Class Is will follow next week. There’s a lot to watch for. Is the crisis in railroad customer service getting better? Are railroads closer to becoming adequately staffed? Is the demand environment weakening as inflation and higher interest rates take a toll on the economy? Are supply chain bottlenecks affecting rail fluidity easing? Is the pricing power railroads wielded in recent quarters starting to soften? Any further updates on coal’s momentary demand renaissance? How about nearshoring, the labor situation, the CP-KCS merger, this year’s grain harvest, the state of intermodal markets, the impact of a suddenly stagnant housing market, and so on. Remember too that other industry stakeholders—including the intermodal champion J.B. Hunt this week—will soon report their Q3 financial results, offering insight on rail developments.

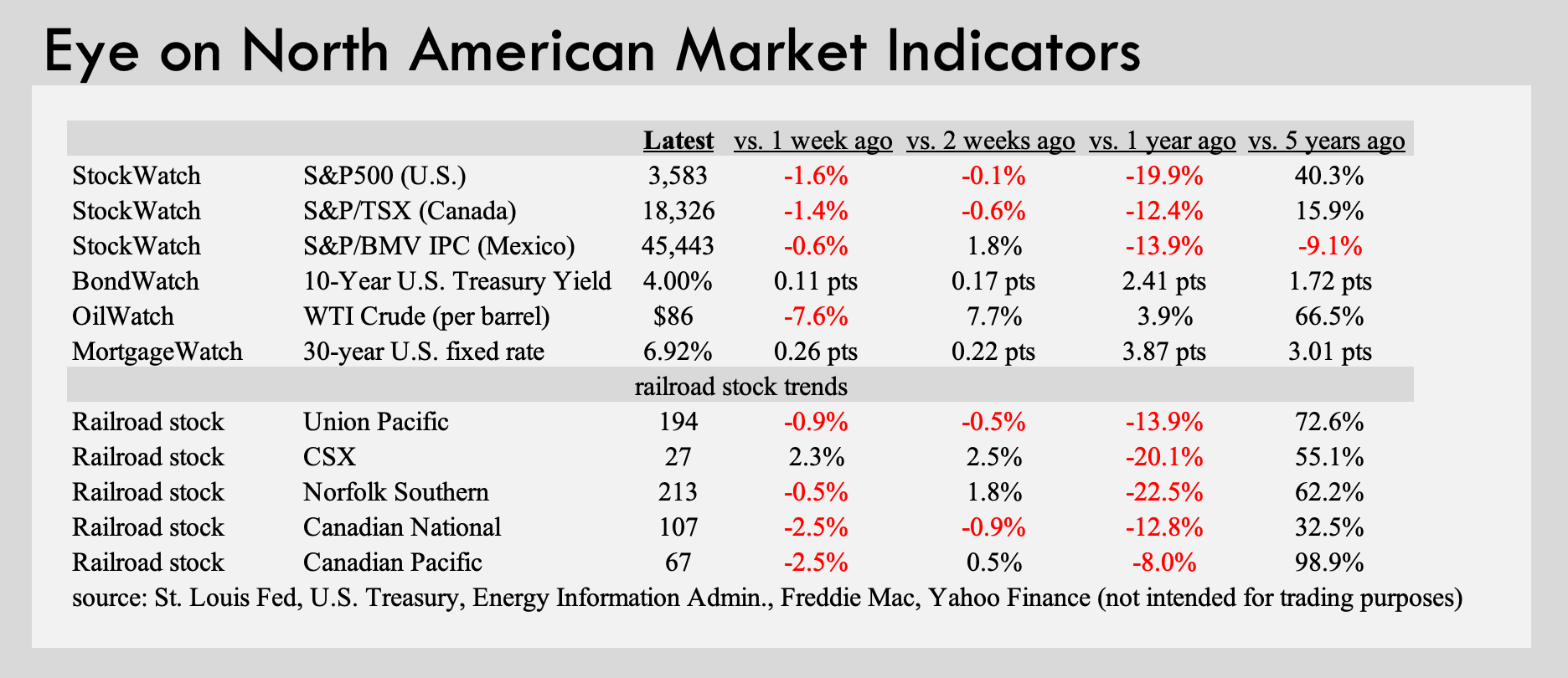

· The economic news continues to worsen on the inflation front. The Labor Department’s September gauge of consumer prices again came in above expectations, rising 0.4% from August. That puts y/y inflation at 8.2%, still far above the Federal Reserve’s 2% target and more reason to think the Fed will continue to raise interest rates. It may sound odd that government officials are deliberately trying to slow the economy. But that’s unfortunately the only tried-and-true method for bringing down prices. Sure enough, the Fed’s tough love approach has dramatically slowed the housing market (which Union Pacific for one has credited for contributing about 5% of its total revenues—think lumber, stone, glass, appliances, roofing, rebar, aggregates, cement, etc.). Consumer retail spending though (see chart), seems to be holding up well, probably thanks to a job market that’s also holding up well.

· Some details of note from the Labor Department’s index of producer prices: Railroad equipment, the latest report shows, saw just a 3% y/y increase in prices during September. However, the cost of moving freight by rail was up 10.7%. If that suggests shippers should avoid the rails, note that annual inflation for shipping by truck now stands at 16.3%.

· Here’s one factor currently pushing up rail pricing in some geographies: an abnormally dry Mississippi River. As the Wall Street Journal reports, that’s “disrupting a vital supply lane for agriculture, oil, and building materials and threatening businesses including barge and towboat operators, farmers and factories.” It adds: “Prices to ship goods have more than doubled in a matter of weeks. Barges are grounding on sandbars in unprecedented numbers and many ports and docks no longer have water deep enough for commercial boats to safely reach them.” Shippers often have no choice but to use rail or highway.

· This from the Journal of Commerce: “BNSF Railway has lowered container backlogs at two inland rail ramps—St. Louis and Fort Worth—as chassis availability increases, allowing more inbound imports to reach both hubs.” This perhaps signals “an easing of inland rail congestion that has resulted in record container dwell times at the ports of Los Angeles and Long Beach.” Separately the Journal of Commerce says truck spot rates are stabilizing after summer declines. As truck pricing rises, shipping by rail becomes more attractive, and vice versa.

· A few updates from the latest AAR traffic data: Through Oct. 8th of this year, U.S. carload traffic is flat y/y, while intermodal traffic is down 5%. Coal, chemicals, and nonmetallic minerals are some key growth areas this year, while grain, metals, forest products, and petroleum are some of the areas of decline. In Canada, this fall’s bumper grain crop is starting to show up in the weekly data, though grain year-to-date is still down 19%. Overall Canadian carload traffic is down 3% year-to-date; intermodal year-to-date is down 2%. In Mexico, meanwhile, 2022 has been a year of growth, thanks in part to metals, vehicles, and intermodal shipments.

· Happy anniversary to a major milestone in U.S. railroad history. On Oct 14th, 1980 (42 years ago last week), President Carter signed the Staggers Act, designed to reinvigorate and restructure an ailing rail sector. It did exactly that over the ensuing four decades, becoming a model for good public policy. Of course, good is not synonymous with perfect, and the industry structure Staggers created does have its critics, including those who lament the pricing power railroads have gained over shippers, through consolidation. Labor unions, for their part, are often critical of the many lost railroad jobs in the post-Staggers era. Some things are indisputable though. For one, today’s U.S. railroads are financially strong. And the country’s freight railroad infrastructure is world-class, funded mostly with private-sector money.

Publisher’s Note: With railroad earnings season now upon us, the next few issues of Railroad Weekly are sure to be action packed! Please consider subscribing if you don’t already. For organizations with multiple readers, discounts are now available. As always contact me with any comments or questions. -Jay (jay@railroadweekly.com).

Connect with me on LinkedIn: https://www.linkedin.com/in/jay-shabat-6477b31/

Labor Update

· As mentioned above, the BMWED-IBT union—one of many voting on whether to accept or reject a new national work contract—voted no. The disappointing news for railroads comes in advance of the larger and more consequential balloting by the industry’s two largest unions, the BLET and SMART-TD. Their balloting is tentatively scheduled to start this week and end Nov. 17th.

· Another union, the SMART-MD, did vote yes last week. So did the smaller National Conference of Firemen & Oilers (NCFO). That makes six unions that have thus far voted to ratify their tentative agreements. Two have rejected them, and three more (including the BLET and SMART-TD) have yet to complete voting.

· As for the BMWED, that’s the Brotherhood of Maintenance of Way Employees, a division of the International Brotherhood of Teamsters (IBT). Their rejection of the tentative contract returns the matter to negotiations and reopens the possibility of a strike. For now, though, both sides agreed to “maintain the status quo” through Nov. 19th. The big BLET/SMART-TD vote will likely prove pivotal—if they vote yes, perhaps the BMWED will go along. The BMWED-IBT is a national union representing workers who build and maintain railroad tracks, bridges, buildings, and other structures. It’s the country’s third largest rail union.

· The BLET, incidentally, held its annual convention in Las Vegas last week, with Labor Secretary Marty Walsh and House Speaker Nancy Pelosi among the speakers. One theme of the event: The threats railroad unions repeatedly cite, including Precision Scheduled Railroading, one-person train crews, and the contracting out of union jobs.

· In a completely separate labor development, Canadian National finalized a three-year contract with the International Brotherhood of Electrical Workers (IBEW). Members will get a 3% wage increase for this year, and another 3% increase in each of the next two years. The IBEW represents approximately 750 unionized signals and communications employees. Annual consumer inflation in Canada by the way, is running at 7%. That was September’s figure, with October’s figure due out on Wednesday.

KCS and the U.S.-Mexico market

· During the CP-KCS merger hearings at the STB last month, KCS chief Pat Ottensmeyer talked about the competitive landscape in the cross-border U.S.-Mexico

Keep reading with a 7-day free trial

Subscribe to Railroad Weekly to keep reading this post and get 7 days of free access to the full post archives.