Earnings Season: Stay Tuned, It’s Starting Soon

Railroad Weekly July 11, 2022

Inside This Issue

· Getting Upsetting? Has Rail Demand Weakened Since Q1 Reporting?

· Labor-Toothed Tiger: Strong Job Market Suggests U.S. Economy Still Strong

· Containers and Trailers: Congestion Still Causing Failures

· Near-Shoring to Mexico: Is It Really Happening?

· Beast of the Northeast: More on the History of Conrail

Track Talk

“On behalf of the undersigned organizations, and the millions of businesses and employees we represent, we are writing to you regarding the ongoing West Coast port labor negotiations between the International Longshore and Warehouse Union and the Pacific Maritime Association. With the contract set to expire today, we urge the administration to continue to work with the parties to reach a new agreement without any disruption to port operations.”

-From a letter to President Biden dated July 1st, signed by roughly 100 U.S.-based trade associations

The Latest

· Anticipation is building as Q2 earnings season approaches. CSX gets things started next Wednesday, followed by Union Pacific on Thursday and then North America’s three other publicly-traded Class I railroads the week after. Their financial results will be largely a sideshow—robust profits have become the norm throughout the sector. Expect more of the same. More closely watched will be their commentary on operations, and whether severe service problems are improving. In short, railroads these days are golden in the eyes of their owners but (hardly for the first time) unloved by their customers, their regulators and their unions. That characterization, to be fair, applies mostly to the U.S. Big Four, namely CSX, UP, Norfolk Southern and Berkshire Hathaway’s BNSF. Canada’s Big Two railroads have separate concerns, including the health of the looming northern grain harvest which last year proved a disaster. Canadian National has a new chief intent on carrying a greater mix of high-margin traffic—when CN last reported results in late April, the demand outlook was rosy for pretty much all its major freight categories (chemicals, plastics, metals, minerals, petroleum, forest products, coal, intermodal, auto, etc.). As for Canadian Pacific, its top strategic focus is of course Kansas City Southern, hoping to finalize what would likely be the last great railroad merger in North America.

· When CN spoke so glowingly and optimistically about demand this spring, it wasn’t alone. The bullishness was generally universal across the rail sector. And the sentiment remained more or less intact through the post-earnings presentations that companies delivered at various investor conferences in May and early June. There hasn’t been much said since then, however, yet the U.S. economy—or parts of it anyway—has unmistakably slowed. Housing sales, for example, suddenly went from scorching hot to nearly frozen, iced by the Federal Reserve’s interest rate hikes to defeat inflation. Consumer spending is still solid but slowing. As recent weeks have passed, it’s been more and more common to hear talk of an imminent U.S. recession—or perhaps one that’s already started.

· The latest U.S. jobs report, however, seems to suggest just the opposite. The economy created another 372,000 jobs in June, not the sort of thing that happens if nationwide production is contracting. Then again, railroads are examples of companies hiring aggressively yet not really growing—they’re just trying to get their existing trains running on time following pandemic-era labor shocks. One interesting and important fact about the national labor force: For all the recent hiring across the economy, the number of Americans currently employed is less than 1% greater than it was in 2019. We’ll soon see what the Class I railroads have to say about all of this.

· One important economic data point to watch this week: The consumer price inflation index for June, coming this Wednesday. Inflation is enemy number one for the Fed, but there are signs that it’s starting to ease. Prices are cooling in areas like commodities, autos and ocean shipping. President Biden, meanwhile, is discussing the removal of some tariffs on Chinese imports, tariffs of which railroads were outspoken opponents when first applied during the Trump presidency.

· In labor matters, still no Presidential announcement on an emergency board addressing the rail industry contract dispute. Still no agreement either in negotiations involving west coast port workers—their old contract expired July 1st, though talks continue. In a matter of less systemic significance, Canadian National struck a deal with its International Brotherhood of Electrical Workers, ending a brief strike that didn’t cause much disruption.

Intermodal Market

· On June 28th, the Intermodal Association of North America (IANA) hosted one of its periodic presentations by Larry Gross, founder and president of Gross Transportation Consulting. He gave his latest thoughts on the intermodal market, starting with the important point that there are really two distinct intermodal markets: domestic and international, each shaped by a unique set of forces. The domestic market (51.5% of the total) is affected by fuel prices, competition with trucks and trends in transload cargo. The international market (48.5%) involves overseas trade, port routings, import strategies and steamship line policies, while also impacted by competition with trucks and trends in transloading.

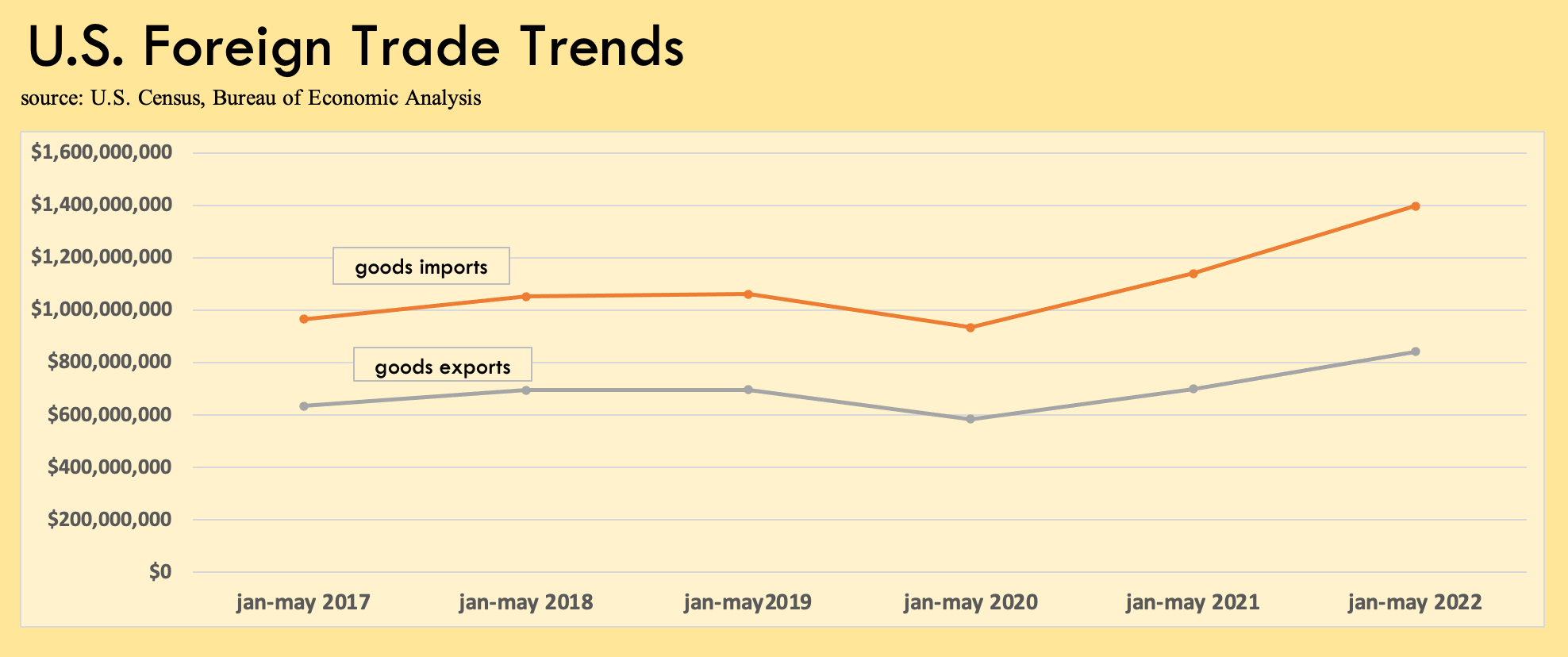

· At mid-year 2022, the international market has grown from earlier in the year but remains significantly smaller than it was a year ago, said Gross. Chassis availability, inland port congestion and other supply side issues remain a constraint on further improvement. Domestic, meanwhile, was expected to improve but hasn’t really done so in recent months. In May more specifically, international movements of containers were down about 9% y/y, while domestic container and trailer movements were up 1%. AAR rail data, Gross adds, doesn’t indicate much sign of upward momentum. He does note that privately-owned containers, rather than rail-owned containers, are becoming a greater share of all activity. Indeed, during May, a record 76% of all domestic container revenue moves took place in those that were privately-owned. Looking at North America’s ports, imports continue to be up sharply y/y while the opposite is true for exports.

Industrial Production in Mexico

· The Financial Times featured an article last week about Mexico’s potential to lure more manufacturing back from Asia. The country is certainly well-positioned, given its geographic proximity to the U.S., its privileged access to U.S. markets, its skilled workforce, its established export sector and indeed, its good transport links to the U.S., including good rail links. When the U.S. slapped heavy tariffs on China during the Trump Administration, Mexico seemed especially well positioned.

· Yet as the FT article makes clear, there’s been no giant sucking sound of factories fleeing to Mexico from Asia. “Between 2018 and 2021 the proportion of manufactured goods imported into the U.S. from Mexico barely changed,” the article explained, citing the consultancy Kearney. Instead, plants moved from mainland China to lower-cost Asian markets like Vietnam and Taiwan. Over that same 2018 to 2021 period, “Asian countries other than China increased their share of U.S. manufactured goods imports from 12.6% to 17.4%.”

· Why not move more to Mexico? Some blame policy. They say President Andrés

Keep reading with a 7-day free trial

Subscribe to Railroad Weekly to keep reading this post and get 7 days of free access to the full post archives.